2025 Sees Slower Insurance M&A Activity Without a ‘Mad Dash’: Insights from OPTIS

In 2025, the landscape of insurance agency mergers and acquisitions saw a notable decline, with a 12% drop compared to the previous year. According to OPTIS Partners, a prominent investment banking and financial consulting firm, the total number of insurance agency deals reached 695 in 2025, down from 787 in 2024.

Despite a notable uptick in activity during the third quarter, the final quarter of 2025 recorded the lowest number of deals—157—since 2019. This figure represents a staggering 47% decrease from the five-year average, as reported by OPTIS Partners’ M&A database.

Tim Cunningham, managing partner at OPTIS, remarked, “For the third consecutive year, there was no mad dash to close deals at year-end. The M&A market continues in a steady, albeit slowing state.” Partner Steve Germundson noted that the distribution of deals was relatively even throughout the year, highlighting that 2019 and 2025 are the only years where Q4 saw lower deal volumes than other quarters.

Among the significant transactions, six firms with revenues exceeding $25 million were sold. Notable acquisitions included Arthur J. Gallagher’s purchase of Assured Partners and Woodruff-Sawyer. Additionally, Risk Strategies and One80 were acquired by Brown & Brown, while The Baldwin Group acquired CAC Group.

Looking ahead, Cunningham expressed optimism, stating, “We expect more large deals and recapitalizations in 2026 as the chase for scale continues. This will continue to benefit the better sellers, whose valuations should remain at their current heady levels, absent a major change in the underlying economy or the insurance marketplace.”

Property and casualty insurance agencies emerged as the primary sellers, accounting for 455 transactions, or 66% of the total deals for the year. Private equity-backed and hybrid buyers maintained their dominance in the market.

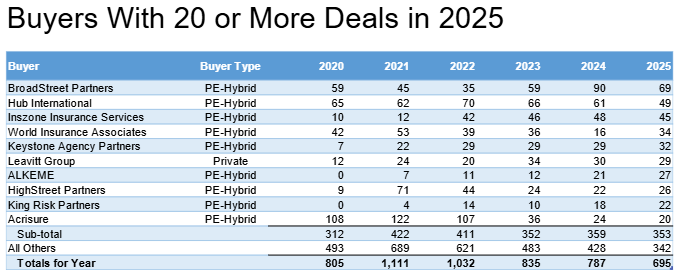

BroadStreet led all buyers in 2025 with 29 acquisitions, although this was a significant decrease from 90 in the previous year. Hub International followed with 49 deals, down from 61 in 2024, while Inszone Insurance Services recorded 45 deals. Both World Insurance Associates and Keystone Agency Partners saw an increase in their deal counts compared to 2024.

OPTIS reported that privately held brokers announced 9% fewer acquisitions, with Leavitt Group being the only firm to make it into the top 10. Publicly held brokers experienced a more significant decline, completing 27% fewer deals in 2025.

According to estimates from OPTIS, there are approximately 30,000 independent insurance agencies with revenues under $1.25 million, most of which lack the capacity for perpetuation. This suggests that consolidation will persist, maintaining deal flow at current levels.

Topics

Mergers & Acquisitions

Interested in Mergers?

Get automatic alerts for this topic.

In 2025, the landscape of insurance agency mergers and acquisitions saw a notable decline, with a 12% drop compared to the previous year. According to OPTIS Partners, a prominent investment banking and financial consulting firm, the total number of insurance agency deals reached 695 in 2025, down from 787 in 2024.

Despite a notable uptick in activity during the third quarter, the final quarter of 2025 recorded the lowest number of deals—157—since 2019. This figure represents a staggering 47% decrease from the five-year average, as reported by OPTIS Partners’ M&A database.

Tim Cunningham, managing partner at OPTIS, remarked, “For the third consecutive year, there was no mad dash to close deals at year-end. The M&A market continues in a steady, albeit slowing state.” Partner Steve Germundson noted that the distribution of deals was relatively even throughout the year, highlighting that 2019 and 2025 are the only years where Q4 saw lower deal volumes than other quarters.

Among the significant transactions, six firms with revenues exceeding $25 million were sold. Notable acquisitions included Arthur J. Gallagher’s purchase of Assured Partners and Woodruff-Sawyer. Additionally, Risk Strategies and One80 were acquired by Brown & Brown, while The Baldwin Group acquired CAC Group.

Looking ahead, Cunningham expressed optimism, stating, “We expect more large deals and recapitalizations in 2026 as the chase for scale continues. This will continue to benefit the better sellers, whose valuations should remain at their current heady levels, absent a major change in the underlying economy or the insurance marketplace.”

Property and casualty insurance agencies emerged as the primary sellers, accounting for 455 transactions, or 66% of the total deals for the year. Private equity-backed and hybrid buyers maintained their dominance in the market.

BroadStreet led all buyers in 2025 with 29 acquisitions, although this was a significant decrease from 90 in the previous year. Hub International followed with 49 deals, down from 61 in 2024, while Inszone Insurance Services recorded 45 deals. Both World Insurance Associates and Keystone Agency Partners saw an increase in their deal counts compared to 2024.

OPTIS reported that privately held brokers announced 9% fewer acquisitions, with Leavitt Group being the only firm to make it into the top 10. Publicly held brokers experienced a more significant decline, completing 27% fewer deals in 2025.

According to estimates from OPTIS, there are approximately 30,000 independent insurance agencies with revenues under $1.25 million, most of which lack the capacity for perpetuation. This suggests that consolidation will persist, maintaining deal flow at current levels.

Topics

Mergers & Acquisitions

Interested in Mergers?

Get automatic alerts for this topic.