Insurance Implications of Rising Global Civil Unrest

A category of insurance risk that hardly existed a little over a decade ago has morphed into a meaningful source of losses for the industry.

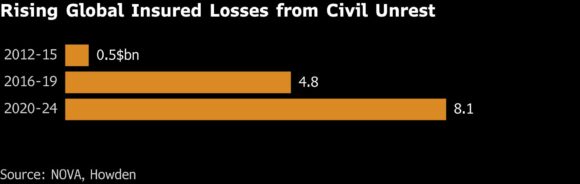

Claims tied to SRCC — strikes, riots, and civil commotion — are emerging as a growing headache for insurers. Episodes of unrest increasingly lead to property destruction in Western democracies. Howden Re estimates that insured losses related to SRCC soared from negligible levels in 2013 to more than $8 billion between 2020 and 2024.

SRCC losses are prone to significant fluctuations from year to year, with single events often altering the landscape dramatically. Following relatively few claims globally in 2025, Howden Re informed Bloomberg that it now expects the US to see a clear increase in SRCC losses this year.

“We live in a time of heightened risk,” said David Flandro, head of industry analysis and strategic advisory at Howden Re. The flare-ups making news headlines in the US are “clearly indicative of a broader trend,” he added.

Civil unrest is on the rise globally, coinciding with a measurable increase in levels of inequality and polarization in some of the world’s wealthiest nations. In many Western countries, the majority of citizens no longer expect to see any growth in generational wealth, according to the Pew Research Center.

Rising political division is exacerbating SRCC risks in both Europe and the US, as noted by Verisk Maplecroft. However, the sharpest increase in protest sizes is occurring in the US, according to their December report.

Read more: Predictive Model Delivers Insights as Insurers, Reinsurers Brace for More Civil Unrest

When ranking countries with the highest SRCC risk, the US stands as the No. 1 Western democracy and is positioned fifth overall, surpassing Pakistan, Bangladesh, and India, based on first-quarter data from Verisk Maplecroft. France ranks seventh. SRCC models consider not only the risk of unrest but also the costs associated with replacing damaged property.

“It’s fair to say that the SRCC risk landscape has fundamentally changed,” stated Torbjorn Soltvedt, associate director of political violence at Verisk.

Historically, insurers offered protection against SRCC at no additional cost. However, the current elevated risk environment is leading to exclusions or restrictions on SRCC coverage in property insurance policies, as noted by Cara Brown, deputy head of terrorism and political violence at insurer Chubb.

SRCC coverage is typically added to other insurance policies, but there’s evidence that the rise in such risks is prompting companies to seek specific coverage. Howden Re reported that insurers began charging “significant additional premiums” for SRCC coverage in 2023, particularly affecting retail assets.

Over two-thirds of multinational corporations are already utilizing political risk modeling tools, a trend that Howden Re indicates is on the rise. In 2024, Lloyd’s of London — the 338-year-old insurance market — assigned SRCC risk its own code. In 2025, Verisk released its first SRCC catastrophe model focused on the US market.

Reinsurer Swiss Re reported that it received only a “couple dozen SRCC claims in the early 2000s, gradually increasing into the hundreds. We have continued to see a couple hundred per year in recent years,” which reflects the market trend.

A Changing US

In the US, several data-tracking services indicate that the number of political protests is on the rise. Meanwhile, perceptions of the US are shifting, according to Stephen M. Davis, senior fellow at Harvard Law School’s program on corporate governance and co-founder of the United Nations’ Principles for Responsible Investment.

Viewing the US as a “safe haven” is becoming a thing of the past, he noted, due to the “policy volatility that now exists,” which is evident both internally and externally.

This sentiment is reflected in markets, as some institutional investors in Europe seek ways to reduce their exposure to the US.

For insurers, accurately calculating loss risks is proving challenging, and Soltvedt emphasizes that protests do not always lead to property damage. For instance, in Minnesota, where Immigration and Customs Enforcement officers killed two US citizens, protests have occurred with “limited direct impacts on commercial property or private property so far,” he stated.

The Trump administration is now retreating from its immigration-enforcement blitz in Minnesota, pulling back after more than two months of operations.

However, given the overall growth in SRCC, the likelihood that a single event could result in losses exceeding $5 billion can no longer be overlooked, according to Verisk Maplecroft. In some regions, SRCC loss risks may even surpass those posed by natural catastrophes.

SRCC as a standalone insurance product “used to be a very niche, small class of business,” remarked Srdjan Todorovic, head of political violence and hostile environment solutions at Allianz Commercial. Yet, a series of significant events in recent years “hit the industry pretty badly and sobered up the market.”

Related:

Copyright 2026 Bloomberg.

Interested in Civil Unrest?

Get automatic alerts for this topic.

A category of insurance risk that hardly existed a little over a decade ago has morphed into a meaningful source of losses for the industry.

Claims tied to SRCC — strikes, riots, and civil commotion — are emerging as a growing headache for insurers. Episodes of unrest increasingly lead to property destruction in Western democracies. Howden Re estimates that insured losses related to SRCC soared from negligible levels in 2013 to more than $8 billion between 2020 and 2024.

SRCC losses are prone to significant fluctuations from year to year, with single events often altering the landscape dramatically. Following relatively few claims globally in 2025, Howden Re informed Bloomberg that it now expects the US to see a clear increase in SRCC losses this year.

“We live in a time of heightened risk,” said David Flandro, head of industry analysis and strategic advisory at Howden Re. The flare-ups making news headlines in the US are “clearly indicative of a broader trend,” he added.

Civil unrest is on the rise globally, coinciding with a measurable increase in levels of inequality and polarization in some of the world’s wealthiest nations. In many Western countries, the majority of citizens no longer expect to see any growth in generational wealth, according to the Pew Research Center.

Rising political division is exacerbating SRCC risks in both Europe and the US, as noted by Verisk Maplecroft. However, the sharpest increase in protest sizes is occurring in the US, according to their December report.

Read more: Predictive Model Delivers Insights as Insurers, Reinsurers Brace for More Civil Unrest

When ranking countries with the highest SRCC risk, the US stands as the No. 1 Western democracy and is positioned fifth overall, surpassing Pakistan, Bangladesh, and India, based on first-quarter data from Verisk Maplecroft. France ranks seventh. SRCC models consider not only the risk of unrest but also the costs associated with replacing damaged property.

“It’s fair to say that the SRCC risk landscape has fundamentally changed,” stated Torbjorn Soltvedt, associate director of political violence at Verisk.

Historically, insurers offered protection against SRCC at no additional cost. However, the current elevated risk environment is leading to exclusions or restrictions on SRCC coverage in property insurance policies, as noted by Cara Brown, deputy head of terrorism and political violence at insurer Chubb.

SRCC coverage is typically added to other insurance policies, but there’s evidence that the rise in such risks is prompting companies to seek specific coverage. Howden Re reported that insurers began charging “significant additional premiums” for SRCC coverage in 2023, particularly affecting retail assets.

Over two-thirds of multinational corporations are already utilizing political risk modeling tools, a trend that Howden Re indicates is on the rise. In 2024, Lloyd’s of London — the 338-year-old insurance market — assigned SRCC risk its own code. In 2025, Verisk released its first SRCC catastrophe model focused on the US market.

Reinsurer Swiss Re reported that it received only a “couple dozen SRCC claims in the early 2000s, gradually increasing into the hundreds. We have continued to see a couple hundred per year in recent years,” which reflects the market trend.

A Changing US

In the US, several data-tracking services indicate that the number of political protests is on the rise. Meanwhile, perceptions of the US are shifting, according to Stephen M. Davis, senior fellow at Harvard Law School’s program on corporate governance and co-founder of the United Nations’ Principles for Responsible Investment.

Viewing the US as a “safe haven” is becoming a thing of the past, he noted, due to the “policy volatility that now exists,” which is evident both internally and externally.

This sentiment is reflected in markets, as some institutional investors in Europe seek ways to reduce their exposure to the US.

For insurers, accurately calculating loss risks is proving challenging, and Soltvedt emphasizes that protests do not always lead to property damage. For instance, in Minnesota, where Immigration and Customs Enforcement officers killed two US citizens, protests have occurred with “limited direct impacts on commercial property or private property so far,” he stated.

The Trump administration is now retreating from its immigration-enforcement blitz in Minnesota, pulling back after more than two months of operations.

However, given the overall growth in SRCC, the likelihood that a single event could result in losses exceeding $5 billion can no longer be overlooked, according to Verisk Maplecroft. In some regions, SRCC loss risks may even surpass those posed by natural catastrophes.

SRCC as a standalone insurance product “used to be a very niche, small class of business,” remarked Srdjan Todorovic, head of political violence and hostile environment solutions at Allianz Commercial. Yet, a series of significant events in recent years “hit the industry pretty badly and sobered up the market.”

Related:

Copyright 2026 Bloomberg.

Interested in Civil Unrest?

Get automatic alerts for this topic.