Berkeley Declares Freedom from Pressure to Implement Uniform Rate Changes

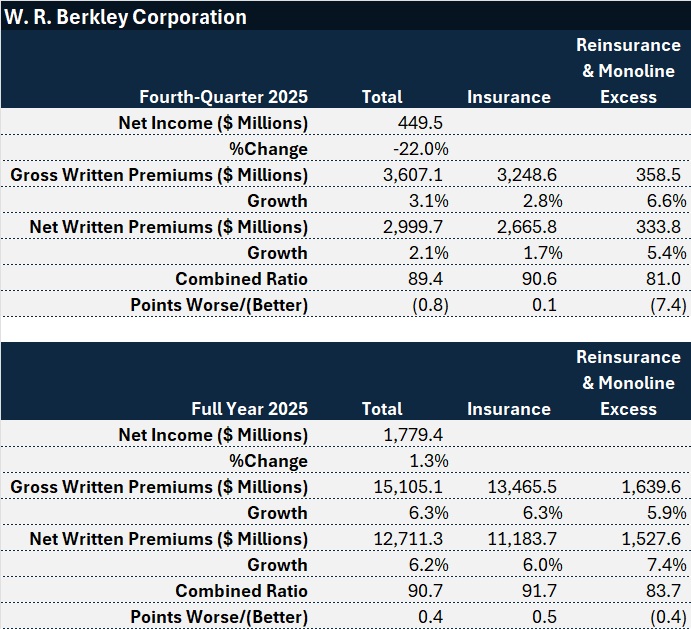

W.R. Berkley recently reported a “flattish” top line but an impressive nearly 15% growth in underwriting income for the fourth quarter of 2025. The insurer’s chief executive hinted at a shift in the trajectory of rate increases moving forward.

During a call with analysts, President and CEO W. Robert Berkley, Jr. noted that while it may be premature to make definitive statements, some recent years appear to be “developing out” favorably. He emphasized that the company is not reducing prior-year loss picks, stating, “We are not feeling, across the board, the same level of pressure to keep pushing on rate.”

Although Berkley opened the call with intriguing insights regarding the use of AI, competition between distributors and carriers, and evolving customer priorities, analysts primarily focused on his comments about the necessity for rate adjustments.

In response to analysts’ inquiries, Berkley highlighted areas where the company has continued to reduce exposures, such as in commercial auto. However, he did not provide much clarification on which lines he considers to have adequate returns to justify less aggressive pricing for 2026. He did mention that other liability business and small-account property present opportunities for the company.

What Berkley Said About Rate Need

Berkley initiated the discussion on rate necessity by advising analysts not to overinterpret the fact that the company’s fourth-quarter 2025 gross written premiums grew only 3% compared to the fourth quarter of 2024, with net premiums increasing by just 2%.

He remarked that the growth figures for October and November were “particularly disappointing—I would call it flattish,” but noted that gross premiums for December rose by 7%, without specifying a breakdown by segment or line of business.

Berkley cautioned against jumping to conclusions based on the quarter’s performance, suggesting that the current situation is likely not the new norm. He indicated that the company is observing some encouraging signs regarding top-line growth as of mid-January.

On the topic of rate specifics, Berkley mentioned that rate growth for lines other than workers’ compensation was just over 7%. He stated, “Given what we’re seeing in some of the more recent years, granted it’s early, but how they seem to be developing out, we are not feeling, across the board, the same level of pressure to keep pushing on rate.” He emphasized that underwriters will remain diligent.

“We will continue to stay on top of it. We are not interested in our margins eroding, but we think that we’re in a pretty good place,” he added.

Berkley noted that two months do not provide a complete picture, but the four-month period through January indicates more top-line growth. He also mentioned that certain segments of their portfolio and parts of the market are showing early returns on loss reserves that suggest a more comfortable position than previously anticipated.

When asked if full-year premium growth, which stood at 6% for 2025, could rise to double digits in 2026, Berkley refrained from making forward-looking projections. However, he expressed optimism that both excess and primary insurance sectors should have opportunities for growth beyond what was observed in the last quarter. In contrast, he noted that the reinsurance market is becoming increasingly challenging.

Regarding loss trends, Berkley stated, “It’s premature to reach any conclusions with confidence, but some of the activity that we are seeing—or lack of activity in some of the more recent years—would suggest that we’re in a comfortable place.” He added, “Trend is a moving target. So, I don’t think it’s that we take our foot off the pedal, but maybe the foot doesn’t have to be stepping down on the pedal quite as hard, selectively….”

The most important insurance news, in your inbox every business day.

Get the insurance industry’s trusted newsletter.

W.R. Berkley recently reported a “flattish” top line but an impressive nearly 15% growth in underwriting income for the fourth quarter of 2025. The insurer’s chief executive hinted at a shift in the trajectory of rate increases moving forward.

During a call with analysts, President and CEO W. Robert Berkley, Jr. noted that while it may be premature to make definitive statements, some recent years appear to be “developing out” favorably. He emphasized that the company is not reducing prior-year loss picks, stating, “We are not feeling, across the board, the same level of pressure to keep pushing on rate.”

Although Berkley opened the call with intriguing insights regarding the use of AI, competition between distributors and carriers, and evolving customer priorities, analysts primarily focused on his comments about the necessity for rate adjustments.

In response to analysts’ inquiries, Berkley highlighted areas where the company has continued to reduce exposures, such as in commercial auto. However, he did not provide much clarification on which lines he considers to have adequate returns to justify less aggressive pricing for 2026. He did mention that other liability business and small-account property present opportunities for the company.

What Berkley Said About Rate Need

Berkley initiated the discussion on rate necessity by advising analysts not to overinterpret the fact that the company’s fourth-quarter 2025 gross written premiums grew only 3% compared to the fourth quarter of 2024, with net premiums increasing by just 2%.

He remarked that the growth figures for October and November were “particularly disappointing—I would call it flattish,” but noted that gross premiums for December rose by 7%, without specifying a breakdown by segment or line of business.

Berkley cautioned against jumping to conclusions based on the quarter’s performance, suggesting that the current situation is likely not the new norm. He indicated that the company is observing some encouraging signs regarding top-line growth as of mid-January.

On the topic of rate specifics, Berkley mentioned that rate growth for lines other than workers’ compensation was just over 7%. He stated, “Given what we’re seeing in some of the more recent years, granted it’s early, but how they seem to be developing out, we are not feeling, across the board, the same level of pressure to keep pushing on rate.” He emphasized that underwriters will remain diligent.

“We will continue to stay on top of it. We are not interested in our margins eroding, but we think that we’re in a pretty good place,” he added.

Berkley noted that two months do not provide a complete picture, but the four-month period through January indicates more top-line growth. He also mentioned that certain segments of their portfolio and parts of the market are showing early returns on loss reserves that suggest a more comfortable position than previously anticipated.

When asked if full-year premium growth, which stood at 6% for 2025, could rise to double digits in 2026, Berkley refrained from making forward-looking projections. However, he expressed optimism that both excess and primary insurance sectors should have opportunities for growth beyond what was observed in the last quarter. In contrast, he noted that the reinsurance market is becoming increasingly challenging.

Regarding loss trends, Berkley stated, “It’s premature to reach any conclusions with confidence, but some of the activity that we are seeing—or lack of activity in some of the more recent years—would suggest that we’re in a comfortable place.” He added, “Trend is a moving target. So, I don’t think it’s that we take our foot off the pedal, but maybe the foot doesn’t have to be stepping down on the pedal quite as hard, selectively….”

The most important insurance news, in your inbox every business day.

Get the insurance industry’s trusted newsletter.