Bermuda Re/Insurers Face Underwriting Profit Decline; M&A Activity Surges Amidst Slowing Organic Growth

Bermuda-based re/insurers monitored by Fitch are projected to experience a decline in underwriting profit in 2025, with an average combined ratio expected to rise to 92%, compared to 90.7% in 2024, according to the ratings agency.

For the first nine months of 2025, Fitch reported that the group of Bermuda re/insurers it tracks achieved solid underwriting profits, posting a combined ratio of 91.0%, an increase from 86.4% during the same period in 2024. (A combined ratio below 100% indicates underwriting profits.)

“This increase in combined ratios was attributed to higher catastrophe losses, slightly less favorable reserve development, and a deterioration in the underlying underwriting result,” Fitch noted. While all companies in the group reported underwriting gains, most experienced a higher combined ratio in 9M 2025 compared to 9M 2024.

The exceptions were AXIS and Aspen, both of which reported combined ratios below 90%, specifically at 89.5%. Fitch monitors nine Bermuda re/insurers, two of which do not report 9M results.

Catastrophe losses are projected to account for approximately 8 percentage points of the 2025 combined ratio, primarily driven by the California wildfires, up from 6.4 points in 2024, as detailed in Fitch Ratings’ “Bermuda Re/Insurance Monitor: 2026.”

The California wildfires in January 2025 resulted in insured losses of US$40 billion and economic losses totaling US$53 billion, with insured losses included in the economic totals.

“The January 2026 reinsurance renewals indicated a significant shift to a buyers’ market, particularly for property risk, which saw its largest rate declines in over a decade,” the Fitch report stated.

“Terms and conditions have marginally loosened, although attachment points and retentions generally remained stable. Pricing decreases in specialty lines were more modest, while casualty lines remained stable as the market continues to manage rising loss costs from social inflation,” the report added.

“Bermuda re/insurers are expected to generate reduced returns in 2025 and 2026, as record high capital levels contribute to a softening market. However, profitability will remain favorable by historical standards,” commented Brian Schneider, senior director at Fitch Ratings, who was quoted in the report.

Shareholders’ equity grew by 12% in 9M 2025 compared to year-end 2024, driven by underwriting gains, strong investment income, and gains in equity and bond markets. Fitch also noted that return on equity will remain favorable in 2025 at nearly 17%, down slightly from 17.8% in 2024.

M&A Activity Escalates as Organic Growth Wanes

Fitch observed that large-scale mergers and acquisitions (M&A) focused on Bermuda have been limited in recent years due to favorable premium pricing and beneficial terms, which have enhanced organic growth opportunities.

Fitch observed that large-scale mergers and acquisitions (M&A) focused on Bermuda have been limited in recent years due to favorable premium pricing and beneficial terms, which have enhanced organic growth opportunities.

“However, as these organic opportunities have diminished in the softening market, M&A activity has returned in 2025 and is expected to continue into 2026, as companies with accumulated capital seek to acquire other re/insurers,” Fitch explained. Recent transactions include the acquisition of newer companies formed since 2019, international diversification efforts, and ongoing interest from asset managers.

“Consolidation may help moderate competitive pressures as overall capacity is reduced, but Fitch is likely to view negatively any individual deal aimed at achieving greater scale and diversity without a clear strategic rationale,” the report stated.

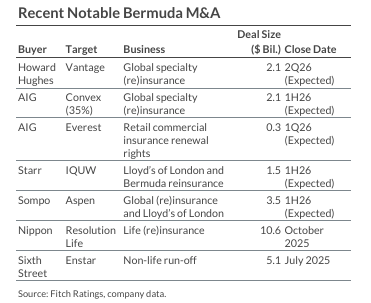

Fitch highlighted notable M&A activity in Bermuda during 2025:

- Vantage Group Holdings announced in December it had agreed to be acquired by Howard Hughes Holdings for US$2.1 billion.

- American International Group (AIG) announced several Bermuda-related transactions in Q4 2025, including an agreement to acquire the renewal rights for a majority of Everest Group’s retail commercial insurance portfolios worldwide for approximately US$300 million.

- AIG also announced it will acquire a 35% equity interest in Convex Group, a privately held global specialty re/insurer.

- In October 2025, Starr International Co. announced it will acquire IQUW Group, a specialty re/insurer backed by private equity firms Aquiline and Abry Partners. IQUW writes at Lloyd’s and operates IQUW Re Bermuda, a reinsurance platform established in 2021.

- In August 2025, Sompo Holdings entered an agreement to purchase 100% of Aspen Insurance Holdings Ltd. for US$3.5 billion (1.3x book value). Apollo Global Management had acquired Aspen in February 2019 for US$2.6 billion (1.1x book value) and currently owns 82.1% of Aspen following its partial IPO in May 2025.

Fitch anticipates that softening market conditions will persist through the midyear 2026 renewals as the competitive environment intensifies. Return on average equity (ROAE) is expected to remain attractive at mid-teen levels as re/insurers continue to exercise discipline in selectively deploying capital.

Fitch maintains a “deteriorating” fundamental sector outlook on global reinsurance and a “neutral” sector outlook on U.S. property/casualty insurance, which includes coverage for Bermuda market re/insurers.

Fitch analyzes nine Bermuda re/insurers: Arch Capital Group Ltd.; Ascot Group Ltd.; Aspen Insurance Holdings Ltd.; AXIS Capital Holdings Ltd.; Everest Group Ltd.; Hamilton Insurance Group Ltd.; PartnerRe Ltd.; RenaissanceRe Holdings Ltd.; and SiriusPoint. (9M data excludes Ascot and PartnerRe as they did not report results).

Topics

Mergers & Acquisitions

Carriers

Profit Loss

Reinsurance

Interested in Carriers?

Get automatic alerts for this topic.

Bermuda-based re/insurers monitored by Fitch are projected to experience a decline in underwriting profit in 2025, with an average combined ratio expected to rise to 92%, compared to 90.7% in 2024, according to the ratings agency.

For the first nine months of 2025, Fitch reported that the group of Bermuda re/insurers it tracks achieved solid underwriting profits, posting a combined ratio of 91.0%, an increase from 86.4% during the same period in 2024. (A combined ratio below 100% indicates underwriting profits.)

“This increase in combined ratios was attributed to higher catastrophe losses, slightly less favorable reserve development, and a deterioration in the underlying underwriting result,” Fitch noted. While all companies in the group reported underwriting gains, most experienced a higher combined ratio in 9M 2025 compared to 9M 2024.

The exceptions were AXIS and Aspen, both of which reported combined ratios below 90%, specifically at 89.5%. Fitch monitors nine Bermuda re/insurers, two of which do not report 9M results.

Catastrophe losses are projected to account for approximately 8 percentage points of the 2025 combined ratio, primarily driven by the California wildfires, up from 6.4 points in 2024, as detailed in Fitch Ratings’ “Bermuda Re/Insurance Monitor: 2026.”

The California wildfires in January 2025 resulted in insured losses of US$40 billion and economic losses totaling US$53 billion, with insured losses included in the economic totals.

“The January 2026 reinsurance renewals indicated a significant shift to a buyers’ market, particularly for property risk, which saw its largest rate declines in over a decade,” the Fitch report stated.

“Terms and conditions have marginally loosened, although attachment points and retentions generally remained stable. Pricing decreases in specialty lines were more modest, while casualty lines remained stable as the market continues to manage rising loss costs from social inflation,” the report added.

“Bermuda re/insurers are expected to generate reduced returns in 2025 and 2026, as record high capital levels contribute to a softening market. However, profitability will remain favorable by historical standards,” commented Brian Schneider, senior director at Fitch Ratings, who was quoted in the report.

Shareholders’ equity grew by 12% in 9M 2025 compared to year-end 2024, driven by underwriting gains, strong investment income, and gains in equity and bond markets. Fitch also noted that return on equity will remain favorable in 2025 at nearly 17%, down slightly from 17.8% in 2024.

M&A Activity Escalates as Organic Growth Wanes

Fitch observed that large-scale mergers and acquisitions (M&A) focused on Bermuda have been limited in recent years due to favorable premium pricing and beneficial terms, which have enhanced organic growth opportunities.

“However, as these organic opportunities have diminished in the softening market, M&A activity has returned in 2025 and is expected to continue into 2026, as companies with accumulated capital seek to acquire other re/insurers,” Fitch explained. Recent transactions include the acquisition of newer companies formed since 2019, international diversification efforts, and ongoing interest from asset managers.

“Consolidation may help moderate competitive pressures as overall capacity is reduced, but Fitch is likely to view negatively any individual deal aimed at achieving greater scale and diversity without a clear strategic rationale,” the report stated.

Fitch highlighted notable M&A activity in Bermuda during 2025:

- Vantage Group Holdings announced in December it had agreed to be acquired by Howard Hughes Holdings for US$2.1 billion.

- American International Group (AIG) announced several Bermuda-related transactions in Q4 2025, including an agreement to acquire the renewal rights for a majority of Everest Group’s retail commercial insurance portfolios worldwide for approximately US$300 million.

- AIG also announced it will acquire a 35% equity interest in Convex Group, a privately held global specialty re/insurer.

- In October 2025, Starr International Co. announced it will acquire IQUW Group, a specialty re/insurer backed by private equity firms Aquiline and Abry Partners. IQUW writes at Lloyd’s and operates IQUW Re Bermuda, a reinsurance platform established in 2021.

- In August 2025, Sompo Holdings entered an agreement to purchase 100% of Aspen Insurance Holdings Ltd. for US$3.5 billion (1.3x book value). Apollo Global Management had acquired Aspen in February 2019 for US$2.6 billion (1.1x book value) and currently owns 82.1% of Aspen following its partial IPO in May 2025.

Fitch anticipates that softening market conditions will persist through the midyear 2026 renewals as the competitive environment intensifies. Return on average equity (ROAE) is expected to remain attractive at mid-teen levels as re/insurers continue to exercise discipline in selectively deploying capital.

Fitch maintains a “deteriorating” fundamental sector outlook on global reinsurance and a “neutral” sector outlook on U.S. property/casualty insurance, which includes coverage for Bermuda market re/insurers.

Fitch analyzes nine Bermuda re/insurers: Arch Capital Group Ltd.; Ascot Group Ltd.; Aspen Insurance Holdings Ltd.; AXIS Capital Holdings Ltd.; Everest Group Ltd.; Hamilton Insurance Group Ltd.; PartnerRe Ltd.; RenaissanceRe Holdings Ltd.; and SiriusPoint. (9M data excludes Ascot and PartnerRe as they did not report results).

Topics

Mergers & Acquisitions

Carriers

Profit Loss

Reinsurance

Interested in Carriers?

Get automatic alerts for this topic.