Catastrophe Bond Risk Premia Plunge to Levels Not Seen Since 2022

Investors in catastrophe bonds are currently experiencing a notable decline in risk premia, reaching levels not seen since before Hurricane Ian impacted Florida in 2022. This shift is largely attributed to a surge in fresh capital, which has driven down potential returns.

This insight comes from an analysis conducted by reinsurer Swiss Re, which released its assessment of the insurance-linked securities market on Monday.

“We have seen capital flow into the market that has resulted in spread tightening,” stated Andy Palmer, who oversees ILS structuring for Europe and Asia at Swiss Re, in an interview with Bloomberg News. “Looking ahead, there are sizeable amounts of maturities upcoming—approximately $11 billion in the first half—but we also expect the new issuance pipeline to remain strong.”

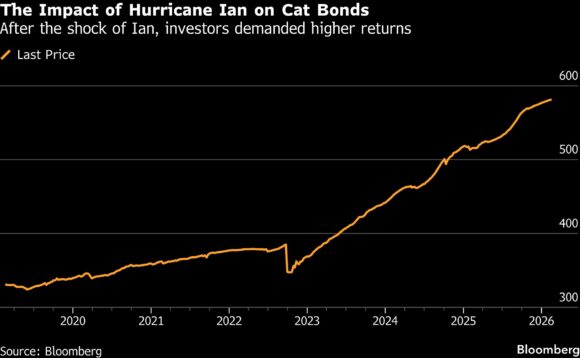

Hurricane Ian marked a significant turning point for the catastrophe bond market. Prior to September 2022, the sector had enjoyed a period characterized by relatively low losses and ample capital, resulting in lower returns. However, the devastation caused by Ian led to a dramatic shift, with risk premia spiking as investors sought higher compensation for holding catastrophe bonds exposed to such risks.

Since then, catastrophe bonds have gained popularity, driven by the increasing frequency of extreme weather events linked to climate change. Reinsurers are increasingly turning to capital markets to manage growing risk levels. Notably, the Swiss Re Global Cat Bond Total Return Index has reported a total return of 61% since 2021, including a record 20% in 2023. In contrast, last year’s gains were around 11%, as the absence of significant losses allowed issuers to offer lower returns.

Investors in catastrophe bonds earn a total return that comprises a risk premium plus the prevailing Treasury rate. Currently, the risk premium stands at approximately 5.2%, which aligns with levels observed in the months leading up to Hurricane Ian in 2022. This is a stark contrast to the roughly 11% available in early 2023.

Moreover, catastrophe bonds have demonstrated resilience during periods of global market volatility, maintaining stability even amid significant events such as US President Donald Trump’s tariff announcements. Swiss Re highlighted that this performance underscores the bonds’ “non-correlation with the broader market,” which has been beneficial during a relatively calm US wind season.

The $60 billion catastrophe bond market is also expanding into new risk classes. A notable development in 2025 was the growing acceptance of wildfire risk among cat bond investors, who had previously considered it too challenging to model.

Read More: Catastrophe Bonds Linked to Wildfires Lose ‘Untouchable’ Status

In a separate report published last week, Howden Capital Markets & Advisory noted that last year’s high issuance levels have solidified catastrophe bonds as “structural anchors” within reinsurance programs.

“What we observed through 2025 and into the January renewals was catastrophe bonds firmly establishing themselves as a core component of clients’ risk management frameworks,” remarked Mitchell Rosenberg, co-head global ILS at HCMA. He emphasized that issuers are now utilizing the market not just to supplement capacity but also to enhance “durability, diversification, and pricing clarity” in their reinsurance strategies.

Top photograph: The destroyed Pine Island Road following Hurricane Ian in Matlacha Isles, Florida, on Oct. 1, 2022. Photo credit: Eva Marie Uzcategui/Bloomberg

Copyright 2026 Bloomberg.

Topics

Catastrophe

Interested in Catastrophe?

Get automatic alerts for this topic.

Investors in catastrophe bonds are currently experiencing a notable decline in risk premia, reaching levels not seen since before Hurricane Ian impacted Florida in 2022. This shift is largely attributed to a surge in fresh capital, which has driven down potential returns.

This insight comes from an analysis conducted by reinsurer Swiss Re, which released its assessment of the insurance-linked securities market on Monday.

“We have seen capital flow into the market that has resulted in spread tightening,” stated Andy Palmer, who oversees ILS structuring for Europe and Asia at Swiss Re, in an interview with Bloomberg News. “Looking ahead, there are sizeable amounts of maturities upcoming—approximately $11 billion in the first half—but we also expect the new issuance pipeline to remain strong.”

Hurricane Ian marked a significant turning point for the catastrophe bond market. Prior to September 2022, the sector had enjoyed a period characterized by relatively low losses and ample capital, resulting in lower returns. However, the devastation caused by Ian led to a dramatic shift, with risk premia spiking as investors sought higher compensation for holding catastrophe bonds exposed to such risks.

Since then, catastrophe bonds have gained popularity, driven by the increasing frequency of extreme weather events linked to climate change. Reinsurers are increasingly turning to capital markets to manage growing risk levels. Notably, the Swiss Re Global Cat Bond Total Return Index has reported a total return of 61% since 2021, including a record 20% in 2023. In contrast, last year’s gains were around 11%, as the absence of significant losses allowed issuers to offer lower returns.

Investors in catastrophe bonds earn a total return that comprises a risk premium plus the prevailing Treasury rate. Currently, the risk premium stands at approximately 5.2%, which aligns with levels observed in the months leading up to Hurricane Ian in 2022. This is a stark contrast to the roughly 11% available in early 2023.

Moreover, catastrophe bonds have demonstrated resilience during periods of global market volatility, maintaining stability even amid significant events such as US President Donald Trump’s tariff announcements. Swiss Re highlighted that this performance underscores the bonds’ “non-correlation with the broader market,” which has been beneficial during a relatively calm US wind season.

The $60 billion catastrophe bond market is also expanding into new risk classes. A notable development in 2025 was the growing acceptance of wildfire risk among cat bond investors, who had previously considered it too challenging to model.

Read More: Catastrophe Bonds Linked to Wildfires Lose ‘Untouchable’ Status

In a separate report published last week, Howden Capital Markets & Advisory noted that last year’s high issuance levels have solidified catastrophe bonds as “structural anchors” within reinsurance programs.

“What we observed through 2025 and into the January renewals was catastrophe bonds firmly establishing themselves as a core component of clients’ risk management frameworks,” remarked Mitchell Rosenberg, co-head global ILS at HCMA. He emphasized that issuers are now utilizing the market not just to supplement capacity but also to enhance “durability, diversification, and pricing clarity” in their reinsurance strategies.

Top photograph: The destroyed Pine Island Road following Hurricane Ian in Matlacha Isles, Florida, on Oct. 1, 2022. Photo credit: Eva Marie Uzcategui/Bloomberg

Copyright 2026 Bloomberg.

Topics

Catastrophe

Interested in Catastrophe?

Get automatic alerts for this topic.