E&S Premium Growth Slows Down Through the First Three Quarters of 2025

The U.S. excess and surplus (E&S) lines market is experiencing a slowdown in growth, with premium increases through September 2025 falling short of the previous year’s figures. This trend marks a significant shift in a sector that has enjoyed years of consistent expansion.

A recent report from AM Best, a prominent insurance industry rating agency, highlights that while the E&S market continues to grow, it is showing signs of tapering off. Premium growth in this sector rose by 9.7% through the third quarter of 2025, a notable decrease from the 13.5% growth observed during the same period the previous year. This slowdown can be attributed to competitive pressures affecting specific lines of coverage, including cyber insurance, commercial property, and directors and officers liability.

According to AM Best, the surplus lines market is expected to stabilize in the near term, yet it will continue to manage a broader array of risks that are more suited for E&S coverage. “These changes have influenced both distribution and product strategies,” stated David Blades, associate director at AM Best. He pointed out that one notable example is the capacity for catastrophe-exposed property coverage. Surplus lines carriers have been able to provide flexibility and customization for risks that no longer align with standard underwriting frameworks.

In recent years, the growth of the E&S market has been significantly driven by newer entrants, particularly fronting companies. However, some of these entities may face challenges due to adverse developments in accident years spanning from 2021 to 2024, where many fronting companies have reportedly concentrated their efforts.

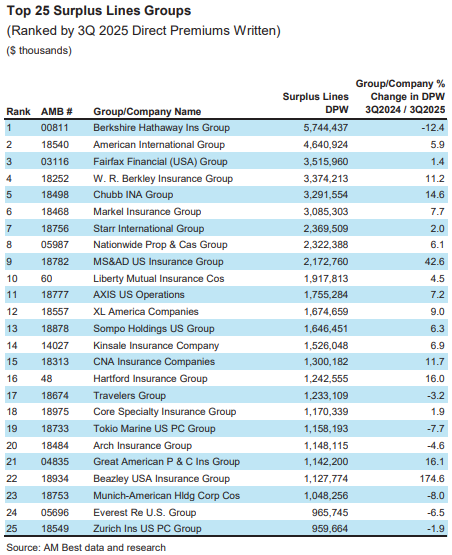

Interestingly, nine of the top ten participants in the E&S market reported an increase in direct premiums written. The exception was Berkshire Hathaway, which saw a decrease of 12.4% in direct premiums written (DPW) during Q3 2025 compared to the same quarter in the prior year.

Topics

Trends

Excess Surplus

Pricing Trends

Was this article valuable?

Here are more articles you may enjoy.

Interested in Excess Surplus?

Get automatic alerts for this topic.

The U.S. excess and surplus (E&S) lines market is experiencing a slowdown in growth, with premium increases through September 2025 falling short of the previous year’s figures. This trend marks a significant shift in a sector that has enjoyed years of consistent expansion.

A recent report from AM Best, a prominent insurance industry rating agency, highlights that while the E&S market continues to grow, it is showing signs of tapering off. Premium growth in this sector rose by 9.7% through the third quarter of 2025, a notable decrease from the 13.5% growth observed during the same period the previous year. This slowdown can be attributed to competitive pressures affecting specific lines of coverage, including cyber insurance, commercial property, and directors and officers liability.

According to AM Best, the surplus lines market is expected to stabilize in the near term, yet it will continue to manage a broader array of risks that are more suited for E&S coverage. “These changes have influenced both distribution and product strategies,” stated David Blades, associate director at AM Best. He pointed out that one notable example is the capacity for catastrophe-exposed property coverage. Surplus lines carriers have been able to provide flexibility and customization for risks that no longer align with standard underwriting frameworks.

In recent years, the growth of the E&S market has been significantly driven by newer entrants, particularly fronting companies. However, some of these entities may face challenges due to adverse developments in accident years spanning from 2021 to 2024, where many fronting companies have reportedly concentrated their efforts.

Interestingly, nine of the top ten participants in the E&S market reported an increase in direct premiums written. The exception was Berkshire Hathaway, which saw a decrease of 12.4% in direct premiums written (DPW) during Q3 2025 compared to the same quarter in the prior year.

Topics

Trends

Excess Surplus

Pricing Trends

Was this article valuable?

Here are more articles you may enjoy.

Interested in Excess Surplus?

Get automatic alerts for this topic.