Florida Reforms Show Clear Impact: Anticipating Further Declines in Reinsurance Rates

Adam Schwebach, broker and head of property for North America at Gallagher Re, recently engaged in an insightful interview with Insurance Journal. This discussion followed Gallagher Re’s annual Florida broker summit, which shed light on the evolving reinsurance market and the ongoing effects of recent legislative reforms in the Sunshine State. The conversation has been lightly edited for clarity and brevity.

IJ: How was the Florida broker event this year?

AS: This was our 11th annual summit. The event brought together a diverse group of Florida carriers, reinsurers, and key stakeholders, including the Florida Office of Insurance Regulation, the Florida Cat Fund, and Citizens (Property Insurance Corp.). The summit aimed to set the stage for the upcoming 6/1 renewals, focusing on topics crucial to the market.

In previous years, the litigation crisis in Florida left little room for optimism. However, following the passage of the 2022 and 2023 litigation reform legislation, there has been a noticeable shift in market sentiment. Initially, reinsurers expressed skepticism about the reforms, recalling past promises that failed to deliver. They adopted a wait-and-see approach to gauge the legislation’s true impact.

While hurricane events are never welcome—especially for residents like myself—there are silver linings. For instance, Hurricane Milton provided valuable test cases, allowing us to compare its impact with previous events. This comparison demonstrated that the recent legislation was indeed transformative, enabling carriers and reinsurers to better assess their exposure and loss potential. The reforms have effectively reduced uncertainty in their models, particularly regarding post-event litigation.

At our summit in January 2025, I would have described the atmosphere as one of cautious optimism. Now, nearly 18 months after Milton, that caution has dissipated. Reinsurers are actively reassessing their underwriting and pricing assumptions, particularly concerning litigation and social inflation, which previously inflated reinsurance costs. This reassessment is expected to positively influence this year’s renewals.

IJ: What are your predictions on the June 1 renewals, compared to Jan. 1?

AS: The January 1 renewals saw rate reductions, and we anticipate similar trends for the mid-year renewals. However, reinsurers are now more proactive in reviewing their pricing assumptions. While this trend may not be as prevalent across the broader U.S. and global reinsurance markets, it is a positive development for Florida.

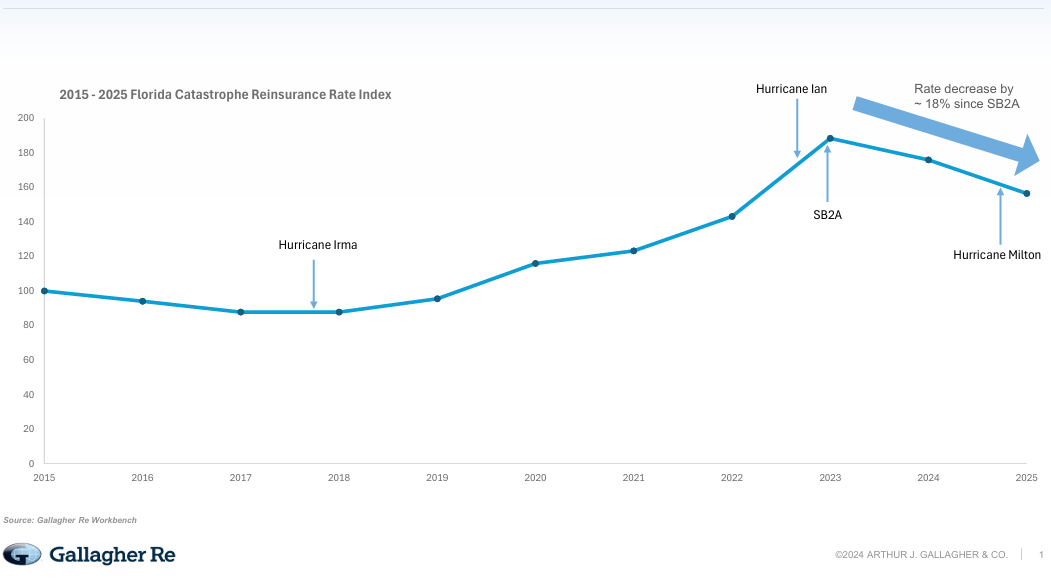

IJ: Over the last decade, how much have reinsurance rates changed in Florida?

AS: Our rate online index indicates that while rates remain elevated compared to the low-water mark of 2017-2018, they have significantly decreased since the peak of the litigation crisis in 2022.

IJ: With rates moderating, are Florida capacity levels balanced, or is the supply of reinsurance now exceeding demand?

AS: Several factors will influence this year’s dynamics. The depopulation of Citizens will shift some reinsurance purchases to the primary market, creating additional demand at the lower end of reinsurance towers. Our analysis indicates that there is ample supply of reinsurance at these levels. Reinsurers are now more willing to consider moving down in reinsurance programs, which is a significant shift from their previous strategy during the litigation crisis.

At the higher end of programs, while capacity is not infinite, there appears to be a robust supply for traditional markets and insurance-linked securities (ILS) markets, which are driving supply and exerting pressure on traditional markets.

IJ: What about the Florida Cat Fund? Are reinsurers concerned about potential changes to its retention?

AS: This topic has been frequently discussed. While some carriers advocate for a lower retention, the fund’s current structure effectively stabilizes the market. The FHCF has never required state funding, making it a significant success story in Florida’s insurance landscape.

IJ: How has Citizens’ depopulation affected reinsurance?

AS: The supply of reinsurance remains strong. Many new carriers are existing ones that have been restructured, which can limit demand. However, the timing is favorable as the reinsurance market softens, allowing for new opportunities. Citizens’ reduction in policies is beneficial for all policyholders, significantly lowering the assessment probability.

IJ: Where do you see the reinsurance market in Florida in five years?

AS: I foresee a focus on stability, which will foster competition and improvement for all stakeholders. Credit is due to the governor’s office and legislators for ensuring that the reforms are maintained, which is crucial for market stability. If uncertainty is minimized, we can hope for a future where reinsurance is no longer a pressing issue in Florida.

IJ: Last year was relatively quiet for hurricanes in Florida. Are reinsurers concerned about potential storms this year?

AS: While last year was quiet in terms of landfalls, the potential for hurricanes remains a reality. As carriers feel more comfortable with their reinsurance levels, we may see them invest their cost savings into additional coverage options, including multiple-events coverage and aggregate coverage, which were previously unavailable. This structural innovation is also being reflected in cat bond offerings, which could influence traditional market strategies.

From 2025: Florida Reinsurance Buyers Found Ample Property Capacity at Mid-Year Renewals

Topics

Florida

Reinsurance

Adam Schwebach, broker and head of property for North America at Gallagher Re, recently engaged in an insightful interview with Insurance Journal. This discussion followed Gallagher Re’s annual Florida broker summit, which shed light on the evolving reinsurance market and the ongoing effects of recent legislative reforms in the Sunshine State. The conversation has been lightly edited for clarity and brevity.

IJ: How was the Florida broker event this year?

AS: This was our 11th annual summit. The event brought together a diverse group of Florida carriers, reinsurers, and key stakeholders, including the Florida Office of Insurance Regulation, the Florida Cat Fund, and Citizens (Property Insurance Corp.). The summit aimed to set the stage for the upcoming 6/1 renewals, focusing on topics crucial to the market.

In previous years, the litigation crisis in Florida left little room for optimism. However, following the passage of the 2022 and 2023 litigation reform legislation, there has been a noticeable shift in market sentiment. Initially, reinsurers expressed skepticism about the reforms, recalling past promises that failed to deliver. They adopted a wait-and-see approach to gauge the legislation’s true impact.

While hurricane events are never welcome—especially for residents like myself—there are silver linings. For instance, Hurricane Milton provided valuable test cases, allowing us to compare its impact with previous events. This comparison demonstrated that the recent legislation was indeed transformative, enabling carriers and reinsurers to better assess their exposure and loss potential. The reforms have effectively reduced uncertainty in their models, particularly regarding post-event litigation.

At our summit in January 2025, I would have described the atmosphere as one of cautious optimism. Now, nearly 18 months after Milton, that caution has dissipated. Reinsurers are actively reassessing their underwriting and pricing assumptions, particularly concerning litigation and social inflation, which previously inflated reinsurance costs. This reassessment is expected to positively influence this year’s renewals.

IJ: What are your predictions on the June 1 renewals, compared to Jan. 1?

AS: The January 1 renewals saw rate reductions, and we anticipate similar trends for the mid-year renewals. However, reinsurers are now more proactive in reviewing their pricing assumptions. While this trend may not be as prevalent across the broader U.S. and global reinsurance markets, it is a positive development for Florida.

IJ: Over the last decade, how much have reinsurance rates changed in Florida?

AS: Our rate online index indicates that while rates remain elevated compared to the low-water mark of 2017-2018, they have significantly decreased since the peak of the litigation crisis in 2022.

IJ: With rates moderating, are Florida capacity levels balanced, or is the supply of reinsurance now exceeding demand?

AS: Several factors will influence this year’s dynamics. The depopulation of Citizens will shift some reinsurance purchases to the primary market, creating additional demand at the lower end of reinsurance towers. Our analysis indicates that there is ample supply of reinsurance at these levels. Reinsurers are now more willing to consider moving down in reinsurance programs, which is a significant shift from their previous strategy during the litigation crisis.

At the higher end of programs, while capacity is not infinite, there appears to be a robust supply for traditional markets and insurance-linked securities (ILS) markets, which are driving supply and exerting pressure on traditional markets.

IJ: What about the Florida Cat Fund? Are reinsurers concerned about potential changes to its retention?

AS: This topic has been frequently discussed. While some carriers advocate for a lower retention, the fund’s current structure effectively stabilizes the market. The FHCF has never required state funding, making it a significant success story in Florida’s insurance landscape.

IJ: How has Citizens’ depopulation affected reinsurance?

AS: The supply of reinsurance remains strong. Many new carriers are existing ones that have been restructured, which can limit demand. However, the timing is favorable as the reinsurance market softens, allowing for new opportunities. Citizens’ reduction in policies is beneficial for all policyholders, significantly lowering the assessment probability.

IJ: Where do you see the reinsurance market in Florida in five years?

AS: I foresee a focus on stability, which will foster competition and improvement for all stakeholders. Credit is due to the governor’s office and legislators for ensuring that the reforms are maintained, which is crucial for market stability. If uncertainty is minimized, we can hope for a future where reinsurance is no longer a pressing issue in Florida.

IJ: Last year was relatively quiet for hurricanes in Florida. Are reinsurers concerned about potential storms this year?

AS: While last year was quiet in terms of landfalls, the potential for hurricanes remains a reality. As carriers feel more comfortable with their reinsurance levels, we may see them invest their cost savings into additional coverage options, including multiple-events coverage and aggregate coverage, which were previously unavailable. This structural innovation is also being reflected in cat bond offerings, which could influence traditional market strategies.

From 2025: Florida Reinsurance Buyers Found Ample Property Capacity at Mid-Year Renewals

Topics

Florida

Reinsurance