Marsh Reports 4% Decline in Q4 Global Commercial Insurance Rates, Marking Sixth Consecutive Quarterly Drop

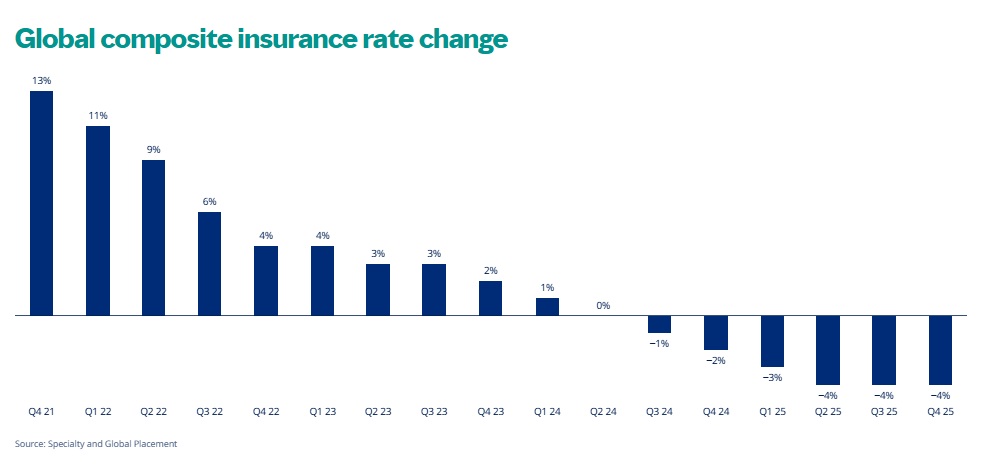

In a notable shift, global commercial insurance rates saw a decline of 4% in the fourth quarter of 2025. This marks the sixth consecutive quarter of decreasing rates following a seven-year period of increases, as reported by the Global Insurance Market Index from Marsh Risk, a division of Marsh.

According to Marsh Risk, the primary factors contributing to this decline include heightened competition among insurers, a favorable loss environment, and favorable reinsurance pricing, alongside increased market capacity. It’s worth noting that Marsh’s index tends to focus on larger account businesses.

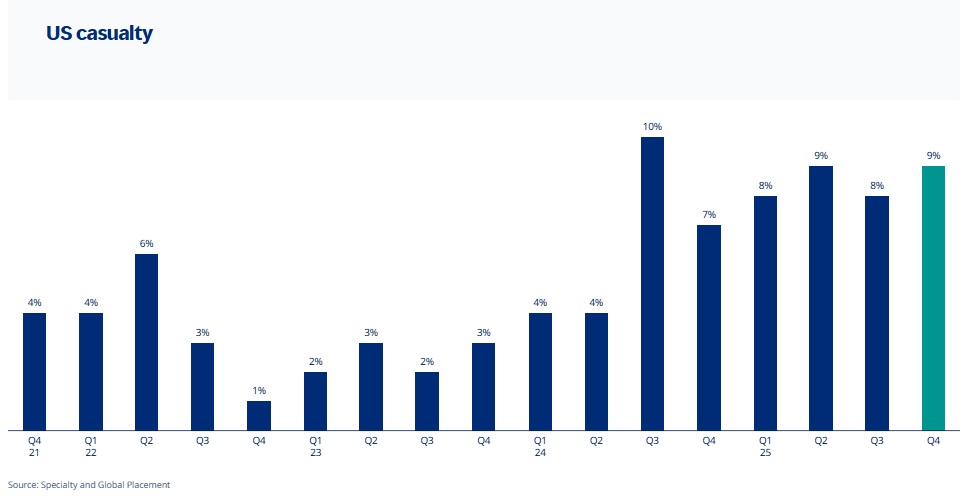

However, the US casualty market presented a contrasting trend, with rates increasing by 9% in Q4 2025, up from 8% in Q3. Additionally, workers’ compensation rates surged by 12%.

Excluding the US, all global regions reported year-over-year composite rate decreases in Q4 2025. The overall composite rate in the US, which had declined by 1% in Q3 2025, remained flat in Q4.

The Pacific region experienced the most significant composite rate decline at 12%, while the IMEA region (India, the Middle East, and Africa) saw an average decrease of 10%. Other regions, including Latin America and the Caribbean (LAC), the UK, and Canada, experienced a 7% decline, while Europe and Asia saw decreases of 6% and 5%, respectively.

“Clients are not only benefiting from declining rates but also from opportunities to negotiate better terms and conditions,” stated John Donnelly, president of Global Placement, in his introduction to the Marsh index. He added that increased competition among insurers is expected to continue.

Donnelly noted that lower reinsurance costs could be a significant factor in the declining rates and increased competition. “Unless there is an exceptionally large catastrophe loss or a series of losses, global rates are likely to keep trending downward,” he remarked.

Marsh indicated that many clients, especially those with favorable risk profiles, have leveraged the competitive environment to negotiate improved terms, enhance coverage, and explore alternative risk transfer solutions such as self-insurance and captives.

Global Product Line Trends

Globally, property rates decreased by 9%, while US property rates fell by 8%, a moderation from the 9% decline in Q3 2025. Marsh attributed this slowdown to renewal timing, noting that the proportion of catastrophe-driven placements with larger rate decreases was lower than in previous periods.

The Pacific region saw the largest decrease in property insurance rates at 14%.

Globally, casualty rates increased by 4%, up from a 3% increase in Q3, driven by a 9% rise in the US, compared to 8% in the previous quarter. Casualty rates in Latin America and the Caribbean remained flat, while other regions experienced decreases ranging from 1% to 9%.

Financial and professional lines (FINPRO) rates decreased by 4% globally, a slight improvement from the 5% decrease in Q3 2025, with declines observed in every region except the US, where rates remained flat. Cyber insurance rates also saw a global decrease of 7%.

“The cyber insurance market is expanding as client demand rises alongside an increase in cyber events,” Donnelly noted, highlighting that more clients are either purchasing cyber coverage for the first time or raising their existing limits. This growth is supported by increased capital from insurers to address escalating risks, intensifying competition and leading to rate declines across all regions.

US Casualty Market

In contrast to the general softening market, the US casualty market experienced rate increases due to ongoing concerns among insurers regarding the frequency and severity of casualty claims, including large jury awards known as “nuclear” verdicts. US casualty insurance rates rose by 9%, while workers’ compensation saw an average increase of 12%.

“Workers’ compensation insurers are focused on rising reserves and medical costs, which could lead to future rate increases,” the report noted. The US umbrella/excess liability market experienced even higher rate hikes than primary lines, with risk-adjusted rate increases of 19%, compared to 16% in Q3. Some insurers limited coverage to a maximum of $10 million per risk due to adverse developments in the US litigation environment.

US FINPRO and Cyber Trends

In the US, financial and professional lines rates remained flat after a 2% decrease in the previous quarter. Directors and officers (D&O) liability rates saw a slight increase of 1%, as insurers resisted the significant decreases observed over the past three years.

Cyber insurance rates in the US decreased by 3%, consistent with the prior quarter, marking the 11th consecutive quarter of rate declines. US cyber capacity remained stable, with no additional capacity expected soon; some insurers even withdrew capacity when pricing was deemed inadequate.

Excess cyber insurers increasingly moved down insurance program towers to retain more premium, although high excess layers were generally more challenging to place compared to previous quarters.

*Note: All references to rate and rate movements in this report are averages unless otherwise noted. For ease of reporting, Marsh has rounded all percentages regarding rate movements to the nearest whole number.

Topics

Trends

Commercial Lines

Business Insurance

Pricing Trends

In a notable shift, global commercial insurance rates saw a decline of 4% in the fourth quarter of 2025. This marks the sixth consecutive quarter of decreasing rates following a seven-year period of increases, as reported by the Global Insurance Market Index from Marsh Risk, a division of Marsh.

According to Marsh Risk, the primary factors contributing to this decline include heightened competition among insurers, a favorable loss environment, and favorable reinsurance pricing, alongside increased market capacity. It’s worth noting that Marsh’s index tends to focus on larger account businesses.

However, the US casualty market presented a contrasting trend, with rates increasing by 9% in Q4 2025, up from 8% in Q3. Additionally, workers’ compensation rates surged by 12%.

Excluding the US, all global regions reported year-over-year composite rate decreases in Q4 2025. The overall composite rate in the US, which had declined by 1% in Q3 2025, remained flat in Q4.

The Pacific region experienced the most significant composite rate decline at 12%, while the IMEA region (India, the Middle East, and Africa) saw an average decrease of 10%. Other regions, including Latin America and the Caribbean (LAC), the UK, and Canada, experienced a 7% decline, while Europe and Asia saw decreases of 6% and 5%, respectively.

“Clients are not only benefiting from declining rates but also from opportunities to negotiate better terms and conditions,” stated John Donnelly, president of Global Placement, in his introduction to the Marsh index. He added that increased competition among insurers is expected to continue.

Donnelly noted that lower reinsurance costs could be a significant factor in the declining rates and increased competition. “Unless there is an exceptionally large catastrophe loss or a series of losses, global rates are likely to keep trending downward,” he remarked.

Marsh indicated that many clients, especially those with favorable risk profiles, have leveraged the competitive environment to negotiate improved terms, enhance coverage, and explore alternative risk transfer solutions such as self-insurance and captives.

Global Product Line Trends

Globally, property rates decreased by 9%, while US property rates fell by 8%, a moderation from the 9% decline in Q3 2025. Marsh attributed this slowdown to renewal timing, noting that the proportion of catastrophe-driven placements with larger rate decreases was lower than in previous periods.

The Pacific region saw the largest decrease in property insurance rates at 14%.

Globally, casualty rates increased by 4%, up from a 3% increase in Q3, driven by a 9% rise in the US, compared to 8% in the previous quarter. Casualty rates in Latin America and the Caribbean remained flat, while other regions experienced decreases ranging from 1% to 9%.

Financial and professional lines (FINPRO) rates decreased by 4% globally, a slight improvement from the 5% decrease in Q3 2025, with declines observed in every region except the US, where rates remained flat. Cyber insurance rates also saw a global decrease of 7%.

“The cyber insurance market is expanding as client demand rises alongside an increase in cyber events,” Donnelly noted, highlighting that more clients are either purchasing cyber coverage for the first time or raising their existing limits. This growth is supported by increased capital from insurers to address escalating risks, intensifying competition and leading to rate declines across all regions.

US Casualty Market

In contrast to the general softening market, the US casualty market experienced rate increases due to ongoing concerns among insurers regarding the frequency and severity of casualty claims, including large jury awards known as “nuclear” verdicts. US casualty insurance rates rose by 9%, while workers’ compensation saw an average increase of 12%.

“Workers’ compensation insurers are focused on rising reserves and medical costs, which could lead to future rate increases,” the report noted. The US umbrella/excess liability market experienced even higher rate hikes than primary lines, with risk-adjusted rate increases of 19%, compared to 16% in Q3. Some insurers limited coverage to a maximum of $10 million per risk due to adverse developments in the US litigation environment.

US FINPRO and Cyber Trends

In the US, financial and professional lines rates remained flat after a 2% decrease in the previous quarter. Directors and officers (D&O) liability rates saw a slight increase of 1%, as insurers resisted the significant decreases observed over the past three years.

Cyber insurance rates in the US decreased by 3%, consistent with the prior quarter, marking the 11th consecutive quarter of rate declines. US cyber capacity remained stable, with no additional capacity expected soon; some insurers even withdrew capacity when pricing was deemed inadequate.

Excess cyber insurers increasingly moved down insurance program towers to retain more premium, although high excess layers were generally more challenging to place compared to previous quarters.

*Note: All references to rate and rate movements in this report are averages unless otherwise noted. For ease of reporting, Marsh has rounded all percentages regarding rate movements to the nearest whole number.

Topics

Trends

Commercial Lines

Business Insurance

Pricing Trends