Runoff Specialists: Essential Strategic Allies for Insurers

The insurance industry has a rich history of managing complex long-tail liabilities. Over time, some of these liabilities have become so burdensome that they necessitate specialized runoff solutions. As market conditions evolve, the nature of these runoff transactions and the runoff industry itself have also transformed.

Legacy specialists in the runoff sector perform functions similar to those of traditional insurers or reinsurers in a runoff scenario. However, their primary focus is not on actively underwriting new business; instead, they concentrate on transacting legacy blocks of business.

“The non-life runoff segment has the potential to become a more integral component of insurers’ overall risk management toolkit.”

This specialization allows these firms the flexibility to tackle tasks that may be more burdensome for those actively underwriting. It also positions them as capital partners, evolving beyond traditional runoff transactions.

While the risks associated with these transactions are not unique to the runoff sector, there is a prevailing perception that all runoff business falls into a “bad business” category. Although much of the business in this area may have underperformed historically, these trends do not necessarily predict future performance.

(Editor’s note: The graphics in this article were originally published on Jan. 12 in AM Best’s report titled “Non-Life Run-off – An Evolving Reinsurance Landscape.”)

![]()

Due diligence is essential in this thought process, as the business is being repriced in real-time, involving new assumptions and limits that must be factored into transactions. Runoff specialists also play a crucial role in claims management or oversight of the process.

Claims Management Expertise

Beyond operational relief, runoff acquirers offer significant claims management expertise. Many of these specialists have developed sophisticated claims departments with extensive experience in handling complex litigation, long-tail liabilities, and legacy exposures across various jurisdictions.

Historically, runoff transactions were primarily executed by the largest insurers and reinsurers. However, a distinct class of runoff specialists has emerged, carving out a niche in the insurance ecosystem. Today, these specialists are recognized for their technical sophistication, transactional agility, and ability to provide customized capital solutions.

While many acquired liabilities present challenges to original insurers, specialists gain critical advantages in the transaction process. They can reprice risks, include buffers for adverse developments, and often set explicit caps on liability exposure. This underwriting discipline is bolstered by sophisticated data analytics, accumulated claims experience, and refined reserving methodologies.

Expanding Beyond the Niche Role

AM Best’s recent analytical report on this sector focused on six runoff specialists, including three with direct rating relationships, facilitating more interactive discussions. This dialogue provides insights that are often difficult to replicate with public sources alone, shaping key takeaways from the analysis:

- Runoff specialists have evolved from niche players managing distressed portfolios to strategic partners that help insurers optimize capital, simplify operations, and refocus on core business.

- The global non-life runoff market has become increasingly concentrated, with a few dominant players accounting for most recent transaction activity.

- Runoff specialists act as stabilizing forces in the broader insurance ecosystem, absorbing legacy risks and enabling insurers to maintain agility amid regulatory requirements and capital market volatility.

Much of what we know today about the runoff market originated from the liability crisis of the 1980s. However, prominent standalone runoff carriers did not emerge until the mid-1990s or early 2000s, with the formations of Cavello Bay Reinsurance (Enstar) and Riverstone International.

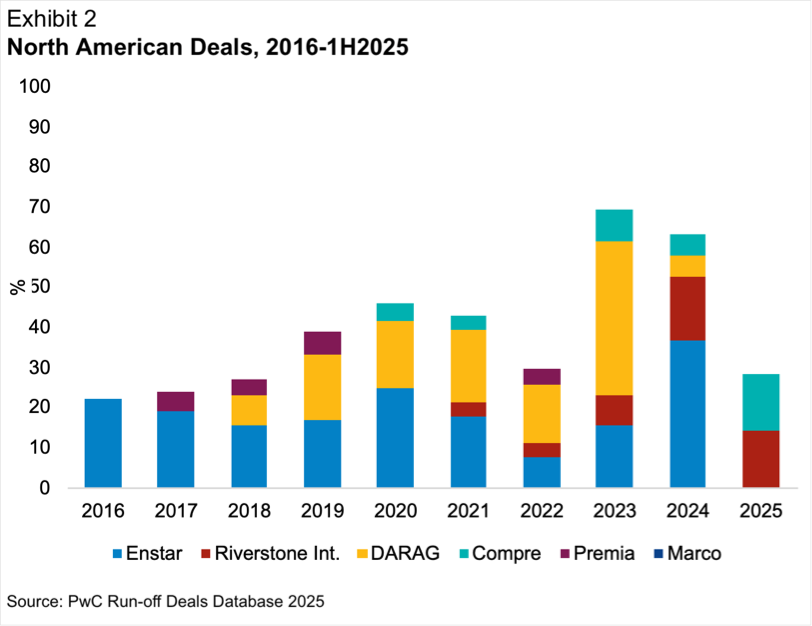

Enstar has been a dominant force in the North American market for nearly a decade, accounting for approximately 20% of all North American non-life runoff transactions since 2016.

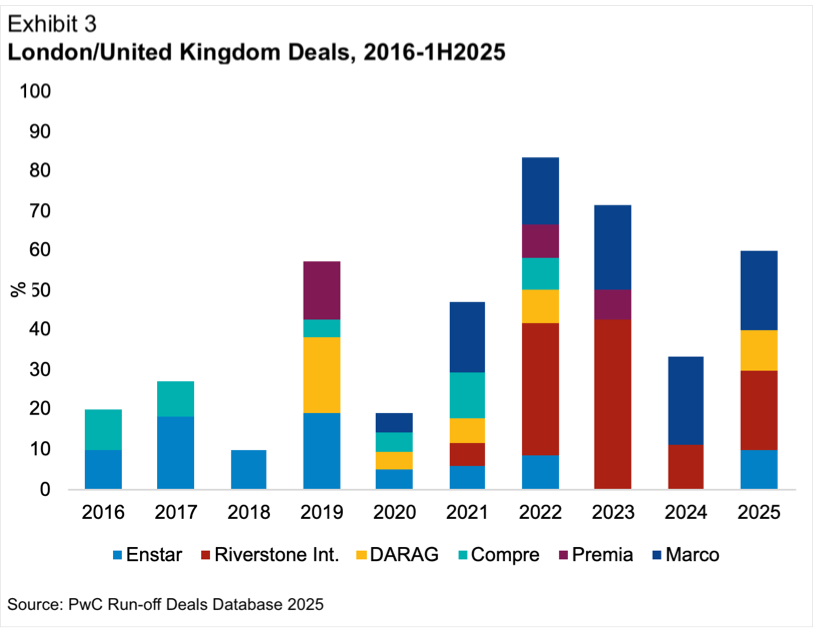

Riverstone has taken a leading position in the United Kingdom and London market, capturing approximately 29% of deal flow since 2022. This concentration may begin to soften as each carrier seeks to diversify its portfolio risk and sustain growth.

The runoff market, as we know it today, is relatively young, existing for only 30 to 50 years compared to the century-plus history of the broader insurance industry. This segment has mastered traditional acquisitions through structured transactions, such as adverse development covers and loss portfolio transfers. However, a wave of young, ambitious talent is eager to evolve and advance this model.

A recent example is Enstar’s acquisition of Accident Fund Holdings Inc., which primarily underwrites workers’ compensation coverage. Enstar has extensive experience managing reserves in this segment and has outperformed the workers’ compensation industry.

What Could Come Next?

AM Best notes that the non-life runoff market has settled into a more defined role in recent years, witnessing both the exit of certain participants and the emergence of new entrants. Despite this turnover, the overall number of active runoff companies has remained relatively stable.

As the perception of legacy solutions shifts away from being associated solely with distressed books of business, the narrative surrounding runoffs is evolving. Recently, runoff platforms have been utilized to provide third-party finality in merger and acquisition transactions and facilitate orderly exits for casualty insurance-linked securities investors. These developments illustrate that legacy solutions can serve broader strategic purposes beyond merely managing problematic reserves.

As the market matures, the non-life runoff segment is poised to become a more integral part of insurers’ overall risk management toolkit. Insurers often invest significant time and resources into designing prospective reinsurance programs, yet retrospective risk management is frequently overlooked until issues arise.

Topics

Carriers

The insurance industry has a rich history of managing complex long-tail liabilities. Over time, some of these liabilities have become so burdensome that they necessitate specialized runoff solutions. As market conditions evolve, the nature of these runoff transactions and the runoff industry itself have also transformed.

Legacy specialists in the runoff sector perform functions similar to those of traditional insurers or reinsurers in a runoff scenario. However, their primary focus is not on actively underwriting new business; instead, they concentrate on transacting legacy blocks of business.

“The non-life runoff segment has the potential to become a more integral component of insurers’ overall risk management toolkit.”

This specialization allows these firms the flexibility to tackle tasks that may be more burdensome for those actively underwriting. It also positions them as capital partners, evolving beyond traditional runoff transactions.

While the risks associated with these transactions are not unique to the runoff sector, there is a prevailing perception that all runoff business falls into a “bad business” category. Although much of the business in this area may have underperformed historically, these trends do not necessarily predict future performance.

(Editor’s note: The graphics in this article were originally published on Jan. 12 in AM Best’s report titled “Non-Life Run-off – An Evolving Reinsurance Landscape.”)

![]()

Due diligence is essential in this thought process, as the business is being repriced in real-time, involving new assumptions and limits that must be factored into transactions. Runoff specialists also play a crucial role in claims management or oversight of the process.

Claims Management Expertise

Beyond operational relief, runoff acquirers offer significant claims management expertise. Many of these specialists have developed sophisticated claims departments with extensive experience in handling complex litigation, long-tail liabilities, and legacy exposures across various jurisdictions.

Historically, runoff transactions were primarily executed by the largest insurers and reinsurers. However, a distinct class of runoff specialists has emerged, carving out a niche in the insurance ecosystem. Today, these specialists are recognized for their technical sophistication, transactional agility, and ability to provide customized capital solutions.

While many acquired liabilities present challenges to original insurers, specialists gain critical advantages in the transaction process. They can reprice risks, include buffers for adverse developments, and often set explicit caps on liability exposure. This underwriting discipline is bolstered by sophisticated data analytics, accumulated claims experience, and refined reserving methodologies.

Expanding Beyond the Niche Role

AM Best’s recent analytical report on this sector focused on six runoff specialists, including three with direct rating relationships, facilitating more interactive discussions. This dialogue provides insights that are often difficult to replicate with public sources alone, shaping key takeaways from the analysis:

- Runoff specialists have evolved from niche players managing distressed portfolios to strategic partners that help insurers optimize capital, simplify operations, and refocus on core business.

- The global non-life runoff market has become increasingly concentrated, with a few dominant players accounting for most recent transaction activity.

- Runoff specialists act as stabilizing forces in the broader insurance ecosystem, absorbing legacy risks and enabling insurers to maintain agility amid regulatory requirements and capital market volatility.

Much of what we know today about the runoff market originated from the liability crisis of the 1980s. However, prominent standalone runoff carriers did not emerge until the mid-1990s or early 2000s, with the formations of Cavello Bay Reinsurance (Enstar) and Riverstone International.

Enstar has been a dominant force in the North American market for nearly a decade, accounting for approximately 20% of all North American non-life runoff transactions since 2016.

Riverstone has taken a leading position in the United Kingdom and London market, capturing approximately 29% of deal flow since 2022. This concentration may begin to soften as each carrier seeks to diversify its portfolio risk and sustain growth.

The runoff market, as we know it today, is relatively young, existing for only 30 to 50 years compared to the century-plus history of the broader insurance industry. This segment has mastered traditional acquisitions through structured transactions, such as adverse development covers and loss portfolio transfers. However, a wave of young, ambitious talent is eager to evolve and advance this model.

A recent example is Enstar’s acquisition of Accident Fund Holdings Inc., which primarily underwrites workers’ compensation coverage. Enstar has extensive experience managing reserves in this segment and has outperformed the workers’ compensation industry.

What Could Come Next?

AM Best notes that the non-life runoff market has settled into a more defined role in recent years, witnessing both the exit of certain participants and the emergence of new entrants. Despite this turnover, the overall number of active runoff companies has remained relatively stable.

As the perception of legacy solutions shifts away from being associated solely with distressed books of business, the narrative surrounding runoffs is evolving. Recently, runoff platforms have been utilized to provide third-party finality in merger and acquisition transactions and facilitate orderly exits for casualty insurance-linked securities investors. These developments illustrate that legacy solutions can serve broader strategic purposes beyond merely managing problematic reserves.

As the market matures, the non-life runoff segment is poised to become a more integral part of insurers’ overall risk management toolkit. Insurers often invest significant time and resources into designing prospective reinsurance programs, yet retrospective risk management is frequently overlooked until issues arise.

Topics

Carriers