The $3 Trillion AI Data Center Expansion Dominates Debt Markets

More than $3 trillion. That’s the staggering price tag to build the data centers needed to prepare for the artificial intelligence boom.

Even the world’s largest technology companies—Amazon.com, Microsoft, and Meta Platforms—are not ready to cover this monumental cost solely with their own funds. The substantial equity investments in private firms like OpenAI and Anthropic fall short of this Industrial Revolution-scale expenditure. While government payments and subsidies can help alleviate some financial pressure, they are not sufficient to cover the entire bill.

So, where will the necessary funds come from? The answer lies in debt markets.

Which markets? All of them.

From blue-chip bonds to junk debt, private credit, and intricate asset-backed pools of loans, the options are vast. “The numbers are like nothing any of us who have been in this business for 25 years have seen,” says Matt McQueen, who oversees global credit, securitized products, and municipal banking at Bank of America Corp. “You have to turn over all avenues to make this work.”

Read more: Data Center Boom Offers Organic Growth Opportunities for Brokers Like Aon, Marsh

Last year, AI-related companies and projects accessed debt markets for at least $200 billion—likely an undercount, as many deals remain private. Projections suggest hundreds of billions in issuance for 2026 alone. This increased demand for capital could elevate borrowing costs across corporate America. Whether you’re an institutional investor or an individual saver, the fixed-income side of your portfolio is becoming increasingly AI-centric.

Simultaneously, stock portfolios are swelling with high-value AI-related stocks. The so-called Magnificent 7, which includes Alphabet, Apple, Nvidia, and Tesla, now represents about a third of the S&P 500’s value. This trend complicates diversification. “Portfolio managers will need to determine what level of AI exposure they’re willing to accept,” notes JPMorgan Chase & Co. credit strategist Tarek Hamid. “Your bond portfolio, which historically correlated more with rates and bank performance, is now increasingly linked to technology companies’ performance.”

Despite the risks, credit investors and lenders find AI hard to resist. Conservative estimates from Morgan Stanley and Moody’s Ratings suggest capital expenditures will exceed $3 trillion in the coming years, while JPMorgan anticipates over $5 trillion in spending for the data center and AI boom, including related power supplies.

Borrowers are eager to build—and they want to do it now. This urgency means they are willing to offer attractive rates to lenders. Morgan Stanley predicts $250 billion to $300 billion in issuance in 2026 from just the “hyperscalers”—tech giants like Microsoft and Meta that are expanding computing capacity requiring gigawatts of power. This surge could push the overall investment-grade bond market to record-high volumes in 2026.

While many AI-related dreams sound futuristic, the companies entering this space appear less speculative than the dot-com startups of the past. Corporate bond investors find comfort in the blue-chip status of these hyperscalers. “Most of the investment is backed by companies with profitable existing lines of business that are unlikely to disappear as they invest in this new growth area,” explains John Medina, senior vice president at Moody’s Ratings.

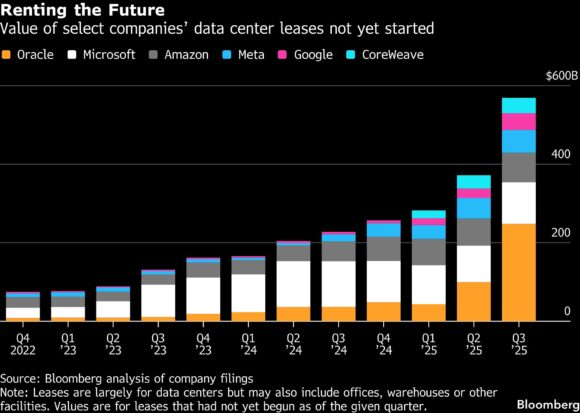

Beyond corporate bonds, a myriad of loans blends features found in real estate debt and construction project finance. The AI infrastructure boom essentially revolves around acquiring land, constructing buildings, connecting them to power, and securing tenants for leases. Developers leverage these leases to assure fixed-income investors of a data center’s creditworthiness. A prime example is Beignet, a $30 billion deal to finance the construction of a Meta data center in Louisiana.

The debt is not recorded on Meta’s balance sheet; instead, it is payable by a special purpose vehicle (SPV) established for the deal, which will repay the loan from its long-term lease with Meta. “The investment-grade market has never seen this level of issuance to fund capital expenditures,” states John Hines, global head of investment-grade debt capital markets at Wells Fargo & Co. “This results in a convergence of asset classes in both public and private markets where investors will shift to where they see the most value.”

However, the lending boom carries inherent risks. What if the demand for AI does not materialize as anticipated? If revenue does come in, but at a slower pace, AI firms—traditionally reliant on internal cash flows—may face higher leverage, amplifying shocks and impacting the health of financial intermediaries, according to a recent bulletin from the Bank for International Settlements.

“There’s a belief that if you can build a data center, the demand is so high that you can’t lose—it’s like selling beer to sailors,” remarks Andrew Kleeman, co-head of private fixed income for SLC Management. “But with any truly innovative technology, there’s often a massive overinvestment followed by a correction.”

Some project finance-style deals are structured for repayment over the loan’s life, while others require repayment mostly at the end, necessitating refinancing. If AI doesn’t revolutionize the world as quickly as hoped, borrowers may struggle to find refinancing participants when the debt comes due. This could lead to rising borrowing costs, impacting revenue streams, or even bankruptcy.

Additionally, rapid advancements in technology pose a risk. A data center built today may quickly become obsolete, long before the debt is repaid. Lease renewals could also become challenging, as lenders prefer long-term leases that align with debt maturity. If today’s build-out results in oversupply, landlords may find it difficult to secure new tenants.

Moreover, lenders risk becoming overexposed to a few companies. Banks are already facing counterparty risk with Oracle Corp., which has backed significant project finance loans with leases. Portfolio managers typically limit their investments in a single business or sector.

Operational risks also loom large. The U.S. is experiencing a shortage of skilled workers and supplies due to the rapid pace of data center construction. Some leases allow tenants to exit contracts if delays occur. Lenders’ exposure to AI could also shift to power plants, as access to power is a significant bottleneck in creating data centers.

As the landscape of lending evolves, the complexity of these financial instruments increases. Understanding the extent of exposure to AI across various portfolios becomes more challenging.

Investment-Grade Bonds

In 2025, Alphabet, Amazon.com, Meta, and Oracle borrowed $93 billion in the U.S. investment-grade corporate bond market, representing about 6% of all debt issued that year. The approximately $8 trillion market absorbed this initial wave of AI-related issuance, but more is anticipated. JPMorgan projects around $300 billion in AI- and data-center-related deals annually for the next five years.

The U.S. investment-grade bond market is one of the most substantial sources of capital globally, making it essential for funding the AI build-out. However, not all hyperscalers are viewed equally. Oracle is considered riskier due to its higher debt relative to earnings and its cash-burning AI investments, leading to increased costs and volumes of traded insurance contracts against its debt.

High-Yield Bonds And Leveraged Loans

These markets, totaling about $3 trillion in the U.S., cater to riskier companies. Last year, three junk bond deals worth approximately $7 billion were sold to finance specific new data centers. While investment-grade companies issued debt with coupons around 4% to 4.5% for five-year notes, high-yield issuers had to pay about 7% to 9%.

Other AI-related companies, like xAI Corp., raised $5 billion in bonds and loans to fund data center construction, with fixed-rate portions bearing a coupon of 12.5%. Morgan Stanley anticipates about $20 billion in AI-related deals in leveraged finance markets in 2026, while JPMorgan projects $150 billion over the next five years.

Convertible Bonds

Convertible bonds, which blend debt and equity, allow companies to borrow with the option to convert debt into equity if stock prices rise. This potential for equity upside results in lower borrowing costs. CoreWeave sold a $2.25 billion convertible bond in December with a coupon of just 1.75%. However, if the equity price does not appreciate, the company will need to refinance or repay the debt.

Project Finance Loans

To avoid excessive debt, hyperscalers often collaborate with developers who construct data centers owned by an SPV. The hyperscaler signs a lease with the SPV, which borrows the debt for construction. This structure allows investors to lend against the project itself, ring-fencing assets in case of bankruptcy. In 2025, data-center-related loans accounted for about $170 billion of the market’s roughly $950 billion in debt issuance, a 57% increase from the previous year.

Structured Finance

In structured finance, loans or receivables are pooled and sliced into different risk levels for bond investors. This setup requires consistent cash flows from underlying assets to pay interest. Commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS) can securitize data center debt. JPMorgan projects annual data center securitization issuance could reach $30 billion to $40 billion in 2026 and 2027, representing 7% to 10% of combined issuance in those years.

Beignet Bonds

The Meta Beignet deal stands out as a unique project finance loan. Morgan Stanley arranged over $27 billion of debt, with Pacific Investment Management Co. as the anchor investor, and about $2.5 billion of equity from Blue Owl Capital Inc. for the construction of the Hyperion data center campus. This complex structure allowed Meta to raise funds off balance sheet, backed by a lease and a residual value guarantee.

Private Placements

Insurance companies, the primary lenders in this market, seek deals that match the duration of their liabilities. Lending against a lease from a highly rated hyperscaler for a data center is particularly appealing. “We’ve been investing in data centers for years, so this isn’t new to us,” says Laura Parrott, head of private fixed income at Nuveen.

Private Credit

In private credit, asset managers lend directly to companies or data center projects. They can finance the AI build-out through various avenues, with over $200 billion in outstanding private credit loans to AI-related companies. This figure could rise to $300 billion to $600 billion by 2030, according to the Bank for International Settlements.

GPU Finance

Beyond constructing buildings, companies need microchips, typically GPUs, to fill them. Valor Equity Partners sought to arrange about $20 billion for an SPV to acquire Nvidia processors for xAI’s Colossus 2 project. “There’s going to be a significant demand for financing GPUs,” notes Nasir Khan, head of real assets and global trade at Natixis CIB.

The maturity of such debt usually aligns with the expected depreciation of the chips. For debt investors, lease payments are crucial for covering interest and repaying the debt. However, as the technology evolves, the risk becomes more speculative.

—With Jeannine Amodeo, Carmen Arroyo, Laura Benitez, Pablo Mayo Cerqueiro, Brody Ford, Bailey Lipschultz, Caleb Mutua, and Abhinav Ramnarayan. Paula Seligson covers private credit and leveraged finance for Bloomberg News in New York.

More than $3 trillion. That’s the staggering price tag to build the data centers needed to prepare for the artificial intelligence boom.

Even the world’s largest technology companies—Amazon.com, Microsoft, and Meta Platforms—are not ready to cover this monumental cost solely with their own funds. The substantial equity investments in private firms like OpenAI and Anthropic fall short of this Industrial Revolution-scale expenditure. While government payments and subsidies can help alleviate some financial pressure, they are not sufficient to cover the entire bill.

So, where will the necessary funds come from? The answer lies in debt markets.

Which markets? All of them.

From blue-chip bonds to junk debt, private credit, and intricate asset-backed pools of loans, the options are vast. “The numbers are like nothing any of us who have been in this business for 25 years have seen,” says Matt McQueen, who oversees global credit, securitized products, and municipal banking at Bank of America Corp. “You have to turn over all avenues to make this work.”

Read more: Data Center Boom Offers Organic Growth Opportunities for Brokers Like Aon, Marsh

Last year, AI-related companies and projects accessed debt markets for at least $200 billion—likely an undercount, as many deals remain private. Projections suggest hundreds of billions in issuance for 2026 alone. This increased demand for capital could elevate borrowing costs across corporate America. Whether you’re an institutional investor or an individual saver, the fixed-income side of your portfolio is becoming increasingly AI-centric.

Simultaneously, stock portfolios are swelling with high-value AI-related stocks. The so-called Magnificent 7, which includes Alphabet, Apple, Nvidia, and Tesla, now represents about a third of the S&P 500’s value. This trend complicates diversification. “Portfolio managers will need to determine what level of AI exposure they’re willing to accept,” notes JPMorgan Chase & Co. credit strategist Tarek Hamid. “Your bond portfolio, which historically correlated more with rates and bank performance, is now increasingly linked to technology companies’ performance.”

Despite the risks, credit investors and lenders find AI hard to resist. Conservative estimates from Morgan Stanley and Moody’s Ratings suggest capital expenditures will exceed $3 trillion in the coming years, while JPMorgan anticipates over $5 trillion in spending for the data center and AI boom, including related power supplies.

Borrowers are eager to build—and they want to do it now. This urgency means they are willing to offer attractive rates to lenders. Morgan Stanley predicts $250 billion to $300 billion in issuance in 2026 from just the “hyperscalers”—tech giants like Microsoft and Meta that are expanding computing capacity requiring gigawatts of power. This surge could push the overall investment-grade bond market to record-high volumes in 2026.

While many AI-related dreams sound futuristic, the companies entering this space appear less speculative than the dot-com startups of the past. Corporate bond investors find comfort in the blue-chip status of these hyperscalers. “Most of the investment is backed by companies with profitable existing lines of business that are unlikely to disappear as they invest in this new growth area,” explains John Medina, senior vice president at Moody’s Ratings.

Beyond corporate bonds, a myriad of loans blends features found in real estate debt and construction project finance. The AI infrastructure boom essentially revolves around acquiring land, constructing buildings, connecting them to power, and securing tenants for leases. Developers leverage these leases to assure fixed-income investors of a data center’s creditworthiness. A prime example is Beignet, a $30 billion deal to finance the construction of a Meta data center in Louisiana.

The debt is not recorded on Meta’s balance sheet; instead, it is payable by a special purpose vehicle (SPV) established for the deal, which will repay the loan from its long-term lease with Meta. “The investment-grade market has never seen this level of issuance to fund capital expenditures,” states John Hines, global head of investment-grade debt capital markets at Wells Fargo & Co. “This results in a convergence of asset classes in both public and private markets where investors will shift to where they see the most value.”

However, the lending boom carries inherent risks. What if the demand for AI does not materialize as anticipated? If revenue does come in, but at a slower pace, AI firms—traditionally reliant on internal cash flows—may face higher leverage, amplifying shocks and impacting the health of financial intermediaries, according to a recent bulletin from the Bank for International Settlements.

“There’s a belief that if you can build a data center, the demand is so high that you can’t lose—it’s like selling beer to sailors,” remarks Andrew Kleeman, co-head of private fixed income for SLC Management. “But with any truly innovative technology, there’s often a massive overinvestment followed by a correction.”

Some project finance-style deals are structured for repayment over the loan’s life, while others require repayment mostly at the end, necessitating refinancing. If AI doesn’t revolutionize the world as quickly as hoped, borrowers may struggle to find refinancing participants when the debt comes due. This could lead to rising borrowing costs, impacting revenue streams, or even bankruptcy.

Additionally, rapid advancements in technology pose a risk. A data center built today may quickly become obsolete, long before the debt is repaid. Lease renewals could also become challenging, as lenders prefer long-term leases that align with debt maturity. If today’s build-out results in oversupply, landlords may find it difficult to secure new tenants.

Moreover, lenders risk becoming overexposed to a few companies. Banks are already facing counterparty risk with Oracle Corp., which has backed significant project finance loans with leases. Portfolio managers typically limit their investments in a single business or sector.

Operational risks also loom large. The U.S. is experiencing a shortage of skilled workers and supplies due to the rapid pace of data center construction. Some leases allow tenants to exit contracts if delays occur. Lenders’ exposure to AI could also shift to power plants, as access to power is a significant bottleneck in creating data centers.

As the landscape of lending evolves, the complexity of these financial instruments increases. Understanding the extent of exposure to AI across various portfolios becomes more challenging.

Investment-Grade Bonds

In 2025, Alphabet, Amazon.com, Meta, and Oracle borrowed $93 billion in the U.S. investment-grade corporate bond market, representing about 6% of all debt issued that year. The approximately $8 trillion market absorbed this initial wave of AI-related issuance, but more is anticipated. JPMorgan projects around $300 billion in AI- and data-center-related deals annually for the next five years.

The U.S. investment-grade bond market is one of the most substantial sources of capital globally, making it essential for funding the AI build-out. However, not all hyperscalers are viewed equally. Oracle is considered riskier due to its higher debt relative to earnings and its cash-burning AI investments, leading to increased costs and volumes of traded insurance contracts against its debt.

High-Yield Bonds And Leveraged Loans

These markets, totaling about $3 trillion in the U.S., cater to riskier companies. Last year, three junk bond deals worth approximately $7 billion were sold to finance specific new data centers. While investment-grade companies issued debt with coupons around 4% to 4.5% for five-year notes, high-yield issuers had to pay about 7% to 9%.

Other AI-related companies, like xAI Corp., raised $5 billion in bonds and loans to fund data center construction, with fixed-rate portions bearing a coupon of 12.5%. Morgan Stanley anticipates about $20 billion in AI-related deals in leveraged finance markets in 2026, while JPMorgan projects $150 billion over the next five years.

Convertible Bonds

Convertible bonds, which blend debt and equity, allow companies to borrow with the option to convert debt into equity if stock prices rise. This potential for equity upside results in lower borrowing costs. CoreWeave sold a $2.25 billion convertible bond in December with a coupon of just 1.75%. However, if the equity price does not appreciate, the company will need to refinance or repay the debt.

Project Finance Loans

To avoid excessive debt, hyperscalers often collaborate with developers who construct data centers owned by an SPV. The hyperscaler signs a lease with the SPV, which borrows the debt for construction. This structure allows investors to lend against the project itself, ring-fencing assets in case of bankruptcy. In 2025, data-center-related loans accounted for about $170 billion of the market’s roughly $950 billion in debt issuance, a 57% increase from the previous year.

Structured Finance

In structured finance, loans or receivables are pooled and sliced into different risk levels for bond investors. This setup requires consistent cash flows from underlying assets to pay interest. Commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS) can securitize data center debt. JPMorgan projects annual data center securitization issuance could reach $30 billion to $40 billion in 2026 and 2027, representing 7% to 10% of combined issuance in those years.

Beignet Bonds

The Meta Beignet deal stands out as a unique project finance loan. Morgan Stanley arranged over $27 billion of debt, with Pacific Investment Management Co. as the anchor investor, and about $2.5 billion of equity from Blue Owl Capital Inc. for the construction of the Hyperion data center campus. This complex structure allowed Meta to raise funds off balance sheet, backed by a lease and a residual value guarantee.

Private Placements

Insurance companies, the primary lenders in this market, seek deals that match the duration of their liabilities. Lending against a lease from a highly rated hyperscaler for a data center is particularly appealing. “We’ve been investing in data centers for years, so this isn’t new to us,” says Laura Parrott, head of private fixed income at Nuveen.

Private Credit

In private credit, asset managers lend directly to companies or data center projects. They can finance the AI build-out through various avenues, with over $200 billion in outstanding private credit loans to AI-related companies. This figure could rise to $300 billion to $600 billion by 2030, according to the Bank for International Settlements.

GPU Finance

Beyond constructing buildings, companies need microchips, typically GPUs, to fill them. Valor Equity Partners sought to arrange about $20 billion for an SPV to acquire Nvidia processors for xAI’s Colossus 2 project. “There’s going to be a significant demand for financing GPUs,” notes Nasir Khan, head of real assets and global trade at Natixis CIB.

The maturity of such debt usually aligns with the expected depreciation of the chips. For debt investors, lease payments are crucial for covering interest and repaying the debt. However, as the technology evolves, the risk becomes more speculative.

—With Jeannine Amodeo, Carmen Arroyo, Laura Benitez, Pablo Mayo Cerqueiro, Brody Ford, Bailey Lipschultz, Caleb Mutua, and Abhinav Ramnarayan. Paula Seligson covers private credit and leveraged finance for Bloomberg News in New York.