US Property/Casualty Sector Achieves $35B YTD Underwriting Gain; Insights on By-Line Premium Growth

Earlier this month, AM Best released its initial financial results for U.S. property/casualty insurers, revealing a remarkable net underwriting gain of $34.9 billion for the first nine months of 2025.

According to Best’s Special Report, titled, “First Look: Nine-Month 2025 US Property/Casualty Financial Results,” this figure marks a significant improvement from the approximately $3.7 billion underwriting profit recorded during the same period in 2024.

In line with an earlier report from Fitch Ratings, AM Best reported an aggregate combined ratio of 94.0 for the first three quarters of 2025, alongside a net written premium growth of just over 5%.

Related article: What to Expect in 2026: U.S. P/C Results More Like 2024

“A 7% increase in net premiums earned was supported by muted catastrophe losses during the third quarter of 2025, which kept incurred losses and loss adjustment expenses (LAE) relatively stable compared to the prior year’s nine-month period,” AM Best noted in its report.

AM Best estimates that catastrophe losses contributed 8.0 points to the nine-month 2025 combined ratio, a decrease from an estimated 8.7 points in the previous year.

Both AM Best and Fitch estimate that $18.0 billion of favorable loss reserve development played a role in the 2025 industry results.

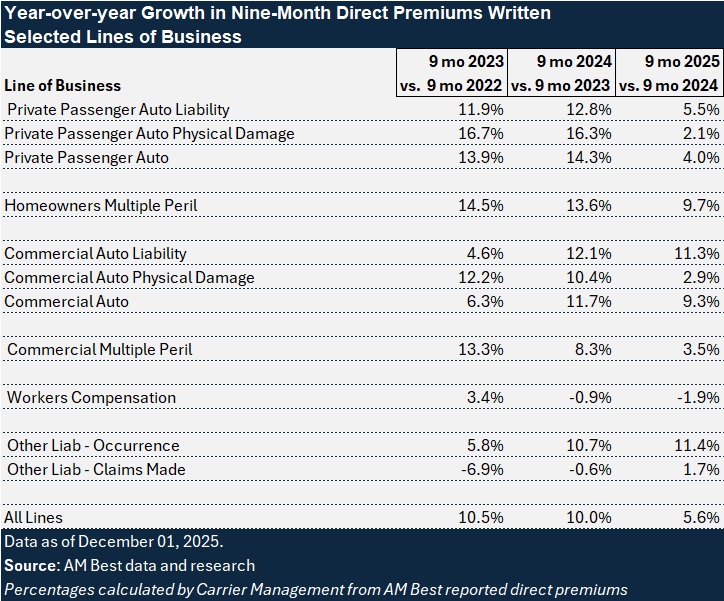

The AM Best report includes detailed tables showing the contributions of loss ratios and expense ratios to the improvement of the combined ratio, primarily driven by a decline in the loss ratio. It also highlights investment and other income contributors to a 6.8% increase in surplus, alongside an overall decline in net income. Additionally, the report provides a line-by-line summary of nine-month direct written premiums for 2025, compared to the same periods in 2022, 2023, and 2024.

Carrier Management has extracted key information from the direct written premium report, showcasing changes in premium growth across several major lines.

Among the selected lines, only commercial auto liability and other liability-occurrence direct premiums maintained double-digit growth for the first nine months of 2025. In contrast, private passenger auto liability growth dropped to 5.5%, a significant decline from the double-digit growth rates seen in 2024 and 2023. Auto physical damage growth has also decreased to between 2% and 3% for both personal and commercial vehicles, while commercial multiple peril growth fell to 3.5%.

Overall, the report indicates a direct premium growth of 5.6% for the first nine months of 2025, compared to a 10% growth rate during the same period in 2024.

Turning to net results, AM Best reported a 5.9% increase in net investment income, combined with the nine-month 2025 underwriting gain, which propelled pretax operating income up by 52% to $102.4 billion for the first nine months of 2025.

Net income stood at $100.9 billion, reflecting a 23% decline from $131.5 billion for the same period in 2024. AM Best attributed this decrease to an 80% reduction in net realized capital gains, primarily driven by a combined $60.5 billion decline at three Berkshire Hathaway companies.

Industry surplus rose by 6.8% from the end of 2024, reaching $1.2 trillion.

The data in the AM Best report is based on nine-month 2025 interim period statutory statements received as of December 1, 2025. These companies represent approximately 98% of total industry net premiums written and 98% of policyholder surplus.

Topics

Trends

USA

Underwriting

Pricing Trends

Property Casualty

Interested in Pricing Trends?

Get automatic alerts for this topic.

Earlier this month, AM Best released its initial financial results for U.S. property/casualty insurers, revealing a remarkable net underwriting gain of $34.9 billion for the first nine months of 2025.

According to Best’s Special Report, titled, “First Look: Nine-Month 2025 US Property/Casualty Financial Results,” this figure marks a significant improvement from the approximately $3.7 billion underwriting profit recorded during the same period in 2024.

In line with an earlier report from Fitch Ratings, AM Best reported an aggregate combined ratio of 94.0 for the first three quarters of 2025, alongside a net written premium growth of just over 5%.

Related article: What to Expect in 2026: U.S. P/C Results More Like 2024

“A 7% increase in net premiums earned was supported by muted catastrophe losses during the third quarter of 2025, which kept incurred losses and loss adjustment expenses (LAE) relatively stable compared to the prior year’s nine-month period,” AM Best noted in its report.

AM Best estimates that catastrophe losses contributed 8.0 points to the nine-month 2025 combined ratio, a decrease from an estimated 8.7 points in the previous year.

Both AM Best and Fitch estimate that $18.0 billion of favorable loss reserve development played a role in the 2025 industry results.

The AM Best report includes detailed tables showing the contributions of loss ratios and expense ratios to the improvement of the combined ratio, primarily driven by a decline in the loss ratio. It also highlights investment and other income contributors to a 6.8% increase in surplus, alongside an overall decline in net income. Additionally, the report provides a line-by-line summary of nine-month direct written premiums for 2025, compared to the same periods in 2022, 2023, and 2024.

Carrier Management has extracted key information from the direct written premium report, showcasing changes in premium growth across several major lines.

Among the selected lines, only commercial auto liability and other liability-occurrence direct premiums maintained double-digit growth for the first nine months of 2025. In contrast, private passenger auto liability growth dropped to 5.5%, a significant decline from the double-digit growth rates seen in 2024 and 2023. Auto physical damage growth has also decreased to between 2% and 3% for both personal and commercial vehicles, while commercial multiple peril growth fell to 3.5%.

Overall, the report indicates a direct premium growth of 5.6% for the first nine months of 2025, compared to a 10% growth rate during the same period in 2024.

Turning to net results, AM Best reported a 5.9% increase in net investment income, combined with the nine-month 2025 underwriting gain, which propelled pretax operating income up by 52% to $102.4 billion for the first nine months of 2025.

Net income stood at $100.9 billion, reflecting a 23% decline from $131.5 billion for the same period in 2024. AM Best attributed this decrease to an 80% reduction in net realized capital gains, primarily driven by a combined $60.5 billion decline at three Berkshire Hathaway companies.

Industry surplus rose by 6.8% from the end of 2024, reaching $1.2 trillion.

The data in the AM Best report is based on nine-month 2025 interim period statutory statements received as of December 1, 2025. These companies represent approximately 98% of total industry net premiums written and 98% of policyholder surplus.

Topics

Trends

USA

Underwriting

Pricing Trends

Property Casualty

Interested in Pricing Trends?

Get automatic alerts for this topic.